In This Article

MicroStrategy’s Bitcoin risks were easy to ignore when the number went up. Now that Strategy (formerly MicroStrategy) sits on 671,268 BTC and trades like a leveraged Bitcoin ETF wearing a Nasdaq ticker, the question won’t go away: Is MicroStrategy a risk for Bitcoin?

The company turned itself into a high-beta, debt-powered Bitcoin vehicle whose balance sheet moves tick-for-tick with the asset it worships. With more than $58-$60 billion in BTC NAV stacked against billions of dollars in market cap and more than $8.24 billion in debt, Strategy isn’t simply a corporate HODLer, it’s a systemic node in Bitcoin’s market structure.

This article breaks down MicroStrategy’s real Bitcoin risks, why Strategy’s balance-sheet engineering matters far beyond its own shareholders, and how one company’s aggressive bet became a shadow system that could amplify Bitcoin volatility rather than dampen it.

Key Takeaways

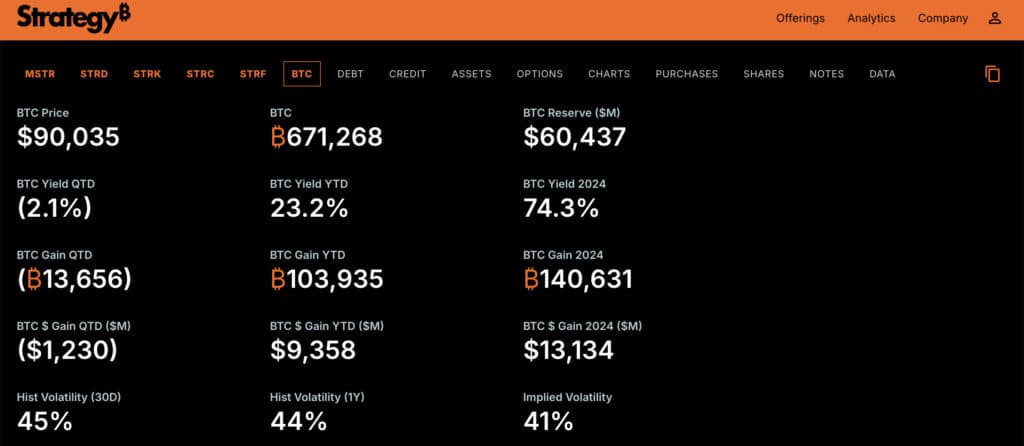

- Strategy (formerly MicroStrategy) holds 671,268 BTC, making it the largest corporate holder of Bitcoin in the world.

- Strategy’s balance sheet is highly sensitive to Bitcoin price volatility, with BTC NAV exceeding its market cap.

- The company uses large amounts of debt, convertible notes, and preferred equity to purchase more Bitcoin, amplifying both upside and downside.

- Index exclusion risk could trigger billions in passive fund outflows, increasing pressure on MSTR stock and liquidity.

- A severe market downturn could force Strategy to sell Bitcoin, creating systemic risk similar to collateral liquidation cascades seen in 2008.

- Leadership concentration around Michael Saylor increases key-person risk as the company continues operating as a leveraged Bitcoin vehicle.

Is Strategy a Risk to Bitcoin: Summary

Strategy’s transformation from a software company into a leveraged Bitcoin balance sheet has created a structural link between MSTR stock, its BTC holdings, and the broader crypto market. With 671,268 BTC financed through debt, convertible bonds, and preferred equity, the company functions more like a high-beta Bitcoin fund than a traditional operating business.

This structure introduces systemic risk. A sharp decline in the Bitcoin price, an unexpected liquidity crunch, or index exclusion that forces billions in passive outflows could pressure Strategy into selling Bitcoin. Such a sale wouldn’t just hit shareholders; it could damage market confidence in the same way collateral failures spread through major indices and institutions in 2008.

The core issue is simple: Strategy magnifies Bitcoin’s upside, but it also amplifies its downside. When a single company controls tens of billions in BTC with leverage, its risk isn’t isolated; it becomes part of Bitcoin’s risk profile.

What is MicroStrategy’s Bitcoin Strategy?

MicroStrategy’s Bitcoin strategy (now operating under the Strategy Inc name) is simple on paper but aggressive in execution: convert excess cash, debt proceeds, and equity capital into Bitcoin and treat BTC as the company’s dominant treasury reserve asset.

Instead of holding cash equivalents that erode under inflation, the company reallocates capital into direct Bitcoin exposure, turning its balance sheet into the largest corporate BTC position on earth. Every quarter, Strategy reinforces the same message: Bitcoin is superior to cash, superior to bonds, and superior to traditional treasury assets.

With 671,268 BTC on the books and over $58-$60 billion in BTC NAV, the company no longer behaves like a standard software business. Strategy is a leveraged Bitcoin vehicle that amplifies BTC movements, a dynamic reflected in MSTR stock price, which regularly exhibits greater volatility than Bitcoin itself.

This makes Strategy’s approach unique but also creates the foundation for MicroStrategy’s Bitcoin risks: high leverage, extreme volatility exposure, and liquidity dependence that tie the company’s fate to Bitcoin’s short-term price cycles.

When the largest corporate holder of Bitcoin becomes the most levered player in the ecosystem, you start to analyze the contagion paths. A forced unwind at Strategy would ripple through Bitcoin markets the way collapsing collateral chains rippled through Wall Street in 2008. Back then it was CDOs. Today it’s corporate BTC balance sheets.

Why MSTR Adopted a Corporate Bitcoin Treasury Strategy?

MicroStrategy adopted a Bitcoin-first corporate treasury model in 2020 as an explicit response to a macro landscape defined by monetary inflation, declining real yields, and stagnating enterprise revenue growth. Michael Saylor framed Bitcoin as a superior long-term asset that would protect shareholder value better than cash or bonds. As stated by Strategy in SEC Form 10-K:

Strategy is the world’s first and largest Bitcoin Treasury Company. We are a publicly traded company that has adopted Bitcoin as our primary treasury reserve asset. By using proceeds from equity and debt financings, as well as cash flows from our operations, we strategically accumulate Bitcoin and advocate for its role as digital capital. Our treasury strategy is designed to provide investors varying degrees of economic exposure to Bitcoin by offering a range of securities, including equity and fixed income instruments.

Instead of hoarding dollars that lose value, Strategy began converting working capital, net proceeds from equity offerings, and funding from convertible debt into Bitcoin. This pivot attracted institutional investors, hedge funds, and macro traders who wanted Bitcoin holdings exposure without dealing with custody or spot-market infrastructure.

But this transition came with structural consequences:

In effect, Strategy repositioned itself as the most highly levered, high-octane version of a Bitcoin ETF, a decision that would draw both admiration and increased scrutiny from analysts and regulators.

How Strategy’s Bitcoin Holdings Work on the Balance Sheet?

Strategy’s balance sheet operates as a Bitcoin engine, with BTC functioning as the company’s dominant asset. The mechanics are straightforward.

Assets:

- The company holds 671,268 BTC as of 29 December.

- These holdings represent more than $58-$60 billion in BTC NAV, dwarfing traditional assets like cash, software revenue, or receivables.

Liabilities:

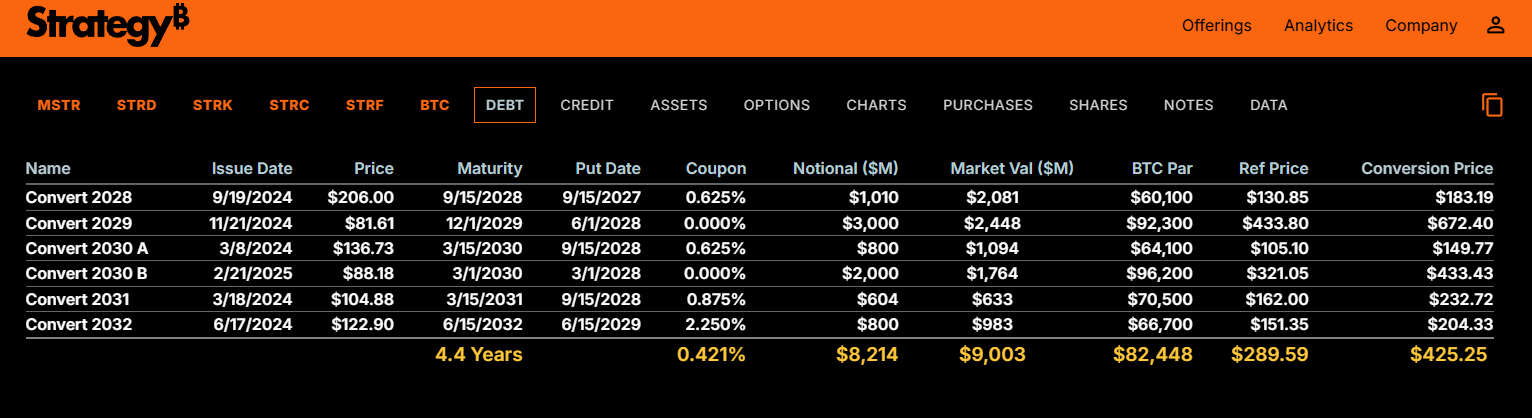

- As of the latest Strategy.com update, the company carries $8.24B in debt and $7.78B in preferred equity.

- Much of this capital was raised explicitly to fund more Bitcoin purchases.

Leverage Ratio:

- Strategy shows 15% leverage, but the real risk isn’t the percentage, it’s the magnitude of exposure relative to equity value and the volatility inherent in BTC.

mNAV & Amplification:

- Strategy’s mNAV of 1.15 signals that the company trades at a premium to its underlying net asset value, meaning shareholders are paying extra for the embedded leverage and future BTC appreciation.

- Its 28% amplification metric highlights how MSTR stock often moves faster than the underlying Bitcoin price.

Income Statement Impact:

- Traditional software revenue plays a shrinking role.

- The company is effectively measured by its BTC holdings, not operational earnings.

- Accounting rules (like impairment) can distort reported results, contributing to sharp swings in reported net asset values.

This structure turns Strategy into a hybrid: part operating business, part leveraged Bitcoin fund. And this hybrid model is precisely why MicroStrategy’s Bitcoin risks carry broader implications. If Bitcoin rises, Strategy outperforms. If Bitcoin falls, Strategy becomes a forced seller, a scenario that could destabilize the broader market.

MicroStrategy’s Bitcoin Risks Explained

Strategy’s pivot from software company to high-beta Bitcoin proxy created a structural imbalance: the company amplified its upside by stacking BTC on the balance sheet, but in doing so, it also hard-wired itself into Bitcoin’s downside mechanics.

The following risks are the core pillars of MicroStrategy’s Bitcoin risks, and they define how exposed both the company and Bitcoin have become to each other.

Bitcoin Price Volatility Risk

Bitcoin is volatile by design; it trades like a global liquidity barometer, not a cash equivalent. For Strategy, this volatility flows directly into:

With 671,268 BTC on the balance sheet, every 1% move in the Bitcoin price shifts Strategy’s BTC NAV by more than half a billion dollars. Bitcoin doesn’t need a black swan to hit the company; a normal 10-20% drawdown is enough to wipe billions from net asset metrics overnight.

Because Strategy acts as the largest corporate holder of Bitcoin, MSTR stock behaves like a leveraged volatility product. When BTC drops faster than expected, institutional traders, quant funds, and even passive investors mark Strategy down harder than Bitcoin itself, widening the volatility gap.

This is why MicroStrategy’s Bitcoin volatility risk is structural. And it’s always one liquidity event away from becoming reflexive.

Market Downturn Risks

A broad market downturn (even one not directly triggered by crypto) magnifies Strategy’s fragility. When liquidity dries up, market participants rotate out of high-beta assets, and Strategy sits at the top of that list.

During these downturns:

Because Strategy now trades like a Bitcoin-tracking equity with leverage, its selloffs amplify pressure on BTC itself. This feedback loop is what makes analysts, including the Bernstein analysts referenced across the industry, flag Strategy as a potential point of systemic risk.

A deep enough market decline could force Strategy into defensive positioning, capital-raising, or in extreme cases, a strategic unwind that resembles how collateralized assets cracked under pressure in 2008.

MicroStrategy’s Bitcoin Liquidity Risk

On paper, Bitcoin is liquid. On a balance sheet loaded with more than half a million BTC, liquidity behaves differently. Three liquidity issues matter most.

1. Scale Liquidity: Strategy owns so much BTC that it cannot exit positions without stressing the market. Even rumors of selling would be enough to rattle institutional investors watching Strategy as a bellwether for direct Bitcoin exposure.

2. Forced Sale Liquidity: If Strategy were pressured to sell Bitcoin due to debt maturities, margin requirements, or deteriorating equity value, the liquidation would hit the market with the force of a systemic shock.

This is the 2008 parallel: In ’08, banks didn’t want to sell mortgage collateral either. But once forced, they triggered a cascade. Bitcoin markets behave the same way when large collateral holders unwind.

3. Balance Sheet Liquidity: Most of Strategy’s assets are BTC. Most of its liabilities are debt, bonds, or preferred equity. This mismatch means the company has very little traditional liquidity like cash, receivables, or working capital, relative to the enormous size of its BTC position.

If Bitcoin enters an extended drawdown while liquidity thins, the Strategy’s ability to meet obligations shrinks. That’s the real MicroStrategy liquidity risk: Not that the company can’t sell BTC, but that selling BTC becomes the worst possible option for the company and for Bitcoin.

MicroStrategy Debt Risk & Leverage Exposure

The foundation of MicroStrategy’s Bitcoin risks is simple: MicroStrategy built the largest corporate Bitcoin position in history by financing it with debt, convertible bonds, and preferred equity.

This leverage gives shareholders amplified upside when the Bitcoin price rises, but it also exposes the company to liquidity stress, refinancing risk, and forced-sale scenarios when markets turn.

With $8.24B in debt and $7.78B in preferred equity listed on Strategy’s official balance sheet, the company has more financial liabilities than most crypto-adjacent firms combined. These instruments were created for one purpose: raise capital at scale and convert that capital into Bitcoin purchases.

This structure makes the Strategy’s balance sheet behave like a collateralized Bitcoin engine. But as any student of 2008 knows, collateral engines work until they don’t. Leverage doesn’t become dangerous when the price rises; it becomes dangerous when liquidity dries up.

How MicroStrategy Uses Debt to Buy Bitcoin?

Strategy raises capital through multiple channels, each one designed to pull cash into the company so it can be converted into BTC holdings:

The strategy is mechanically simple: Raise capital, buy Bitcoin, repeat. But this also means: Liabilities grow, liquidity risk grows, reliance on BTC price grows.

This is the core of microstrategy leveraging Bitcoin. And it’s why analysts view Strategy as the most aggressively levered Bitcoin proxy in the Nasdaq.

Risks of Convertible Notes

Convertible notes are the quiet engine beneath Strategy’s expansion and one of the biggest risk factors buried inside the company’s structure. Here’s why:

1. Conversion Pressure: If MSTR stock falls below conversion thresholds, notes become unattractive to convert, forcing Strategy to repay the debt in cash, not equity. When most of the balance sheet is Bitcoin holdings, not cash, this creates a liquidity mismatch.

2. Refinancing Risk: As notes mature, Strategy must either pay them off, refinance them at higher rates, or sell BTC to meet obligations. In a rising-rate environment or a down Bitcoin cycle, refinancing becomes more expensive, putting more pressure on the balance sheet.

3. NAV Compression: If Strategy trades at a discount to net asset value, issuing new equity becomes less effective, weakening its ability to retire or convert debt.

4. Market Reflexivity: Convertible note holders hedge by shorting MSTR stock, adding downward pressure during drawdowns, especially when volatility spikes.

These dynamics make convertible notes one of the most sensitive points in MicroStrategy’s debt risk, and a key variable in determining whether MicroStrategy can continue scaling its BTC position or get boxed in by the liabilities it created.

Margin Call and Forced Liquidation Risks

Here’s where Strategy’s structure resembles the 2008 mortgage crisis mechanics. You don’t need insolvency to trigger a disaster; you only need collateral impairment paired with falling liquidity. Strategy doesn’t operate on traditional margin like traders on an exchange, but it does face functional equivalents.

1. Debt Servicing Compression: If Bitcoin drops sharply while interest expenses remain fixed, Strategy’s coverage ratios weaken. Cash flow from the software business cannot realistically support billions in liabilities. This is how liquidity stress begins.

2. Equity Value vs. Debt Ratio: If MSTR stock collapses faster than BTC (a recurring pattern) Strategy’s ability to raise new capital dries up. Without new capital, the company may be forced to consider selling Bitcoin to meet obligations. This is the nightmare scenario referenced across the industry: can MicroStrategy be forced to sell Bitcoin? The answer is yes, in specific liquidity crunches, it becomes a real possibility.

3. Downcycle Reflexivity: If passive funds exit due to index exclusion risk, billions in capital could drain from the shareholder base, the exact scenario analysts fear when discussing the $2.8 billion passive-fund exposure figure. Forced selling would hit BTC’s spot liquidity, trigger derivative funding squeezes, and echo the same feedback loops that detonated CDO markets in 2008.

4. Systemic Spillover: Strategy isn’t a random corporate BTC holder; it is the largest corporate holder of Bitcoin. If it’s forced to unwind, the selling pressure could: shock the Bitcoin price, hit institutional traders, disrupt major indices, and damage confidence in corporate Bitcoin adoption.

In other words: One company’s liquidation could become Bitcoin’s contagion event.

Regulatory Risks Facing MicroStrategy

As Strategy Inc. grows into the largest corporate holder of BTC, the company sits under increased scrutiny from U.S. regulators, global policymakers, auditors, and market watchdogs. When your Bitcoin holdings exceed what many sovereign treasuries control, every rule change becomes a potential fault line.

Regulation matters because it affects MicroStrategy’s Bitcoin risks, access to capital, accounting treatment, institutional perception, and even whether major indices continue to classify the company as a software business rather than a direct Bitcoin exposure vehicle. Any adverse shift can influence the stock price, institutional flows, and Strategy’s ability to maintain its leveraged position.

Below are the core regulatory vectors shaping risk for Strategy Inc.

U.S. and Global Crypto Regulation Risks

Strategy operates within the U.S. (still the center of global capital markets) and that creates inherent regulatory exposure. Bitcoin itself has avoided being labeled a security, but that doesn’t mean Strategy avoids oversight. U.S. agencies care about:

As U.S. regulators debate stablecoin rules, exchange registrations, tax reporting, and custody standards, institutional traders increasingly view Bitcoin-heavy corporates as potential spillover channels. That’s where systemic risk enters the conversation.

A future regulatory shift could require stricter disclosures or reclassify Bitcoin-forward companies as financial entities. That would introduce compliance burdens and reshape how passive funds, index providers, and institutional investors treat MSTR stock.

If index committees decide to exclude companies whose balance sheets primarily consist of volatile digital assets, Strategy faces an index exclusion risk that could dislodge billions in passive inflows.

Internationally, MiCA in Europe, the U.K.’s new crypto asset regime, and upcoming APAC rules each tighten standards around corporate digital-asset exposure. If one major jurisdiction forces enhanced capitalization or liquidity buffers for companies with large BTC holdings, Strategy would feel the pressure immediately.

Accounting Risks for Corporate Bitcoin Holdings

The accounting framework is one of the most underrated pieces of Microstrategy Bitcoin investment risk. Under current U.S. GAAP rules, Bitcoin is classified as indefinite-lived intangible property, not a financial instrument. This means: Strategy must write down its Bitcoin when the price falls. But cannot mark it up when the price rises.

The result? A distorted net asset value, understated net asset figures, and income statements that reflect volatility more than economic reality.

Strategy’s filings repeatedly acknowledge that swings in Bitcoin price influence reported earnings, which in turn affect MicroStrategy’s stock, market capitalization, and investor sentiment, even when operational performance is unchanged.

While FASB has introduced fair-value crypto accounting for 2025 onward, the transition period still introduces uncertainty. New rules may require expanded disclosures about custody arrangements, keys, liquidity assumptions, and Bitcoin-backed liabilities. For a company leaning on convertible debt and Bitcoin-dependent capital market access, accounting shifts can influence everything from creditworthiness to refinancing terms.

This is why analysts argue that risks of corporate Bitcoin holdings extend far beyond price volatility; they translate into how the market interprets earnings, liabilities, and operational resilience.

Risks to Strategy’s Core Software Business

Strategy Inc. still operates a long-standing enterprise software business, generating revenue from analytics and cloud-based intelligence tools. But as the company pivots toward Bitcoin, the software arm faces strategic risk.

Key pressures include:

If software revenues decline further, Strategy becomes more dependent on Bitcoin appreciation to maintain its premium, stock valuation, and debt-servicing capacity. That dynamic strengthens the correlation between BTC volatility and MicroStrategy debt risk, creating the same fragility that toppled leveraged firms in traditional finance.

A software business losing momentum becomes a liquidity trap: core operations weaken just as leverage expands.

Leadership Risk and Michael Saylor’s Influence

No analysis of MicroStrategy’s Bitcoin risks is complete without confronting the gravitational force at the centre: Michael Saylor.

Saylor is the architect of the corporate Bitcoin-treasury model. His conviction is absolute, his messaging evangelical, and his willingness to use debt, equity, and net proceeds to acquire more Bitcoin remains unmatched by any public-company CEO.

But this creates concentration risk:

- Investor confidence hinges heavily on Saylor’s reputation.

- His public commentary influences MSTR stock, BTC sentiment, and institutional reactions.

- If Saylor steps down, faces scrutiny, or alters his stance, the market will react instantly.

Strategy Inc. functions, in part, as an extension of Saylor’s identity. That has benefits like strong leadership, clear direction, but also exposes shareholders to personality-driven volatility.

If a future board or regulator challenges Saylor’s aggressive approach, Strategy may be forced to unwind leverage, reduce Bitcoin holdings, or recalibrate capital strategy. For a company built on conviction and leverage, that pivot could be destabilizing.

Conclusion

MicroStrategy, now Strategy Inc., rewired its entire corporate identity around leverage, liquidity, and the assumption that Bitcoin will keep rising faster than debt costs. That transformation created one of the most fascinating balance sheets in public markets, but it also produced a new category of risk: MicroStrategy’s Bitcoin risks, where the company’s fate and Bitcoin’s stability are now partially intertwined.

Strategy’s balance sheet behaves like a levered Bitcoin fund inside a public company wrapper, a structure that works brilliantly when liquidity is cheap and Bitcoin price climbs, but becomes pressure-sensitive during market downturns.

If Strategy ever faces a liquidity crunch, refinancing problem, regulatory shift, or index exclusion event, it could be forced into defensive actions that ripple across the entire market. Bitcoin isn’t dependent on Strategy. But Strategy is dependent on Bitcoin. And in a world where one company controls tens of billions in BTC using leverage, the boundary between corporate risk and systemic risk gets blurry.

See Also:

- Crypto Exchange Promos & Discounts

- 14 Best Crypto Bonuses in 2026

- Who is Shibetoshi Nakamoto (Billy Markus)

- Who is Elon Musk?

- What is DeFAI? A Beginner’s Guide

- Crypto Market Cycles: Are We Still Following 4-Year Pattern?

- What is a Perp DEX? Perpetuals Explained

FAQs

Is MicroStrategy’s Bitcoin strategy risky?

Yes. Strategy Inc. uses leverage, convertible debt, and ongoing equity issuance to buy Bitcoin, which amplifies both gains and losses. Its balance sheet is tied almost entirely to BTC, making the strategy inherently high-risk.

Can MicroStrategy be forced to sell Bitcoin?

While the company intends to never sell, a severe liquidity crunch, debt maturity, or refinancing failure could pressure Strategy into selling part of its BTC stack. It’s unlikely in normal conditions but absolutely possible in extreme ones.

What happens to MicroStrategy if Bitcoin crashes?

A major Bitcoin drawdown would wipe billions from Strategy’s net asset value and put stress on its leveraged capital structure. It could limit access to new capital and raise the risk of dilution or asset sales.

Is MSTR stock more risky than BTC?

Yes. MSTR behaves like a leveraged Bitcoin position, meaning it typically moves more than BTC in both directions. Investors take on Bitcoin volatility plus corporate, debt, and index-classification risk.

How much debt has MicroStrategy taken on for Bitcoin?

Strategy carries more than $8 billion in debt, much of it raised specifically to purchase BTC. This includes senior notes, convertible bonds, and preferred equity.

How secure are MicroStrategy’s Bitcoin holdings?

The BTC itself is professionally custodied and accounted for under updated fair-value rules. The real risk isn’t security, it’s the company’s leverage, liquidity obligations, and dependence on Bitcoin’s price to support its capital structure.

References

- Strategy Inc. “Debt.” Strategy, https://www.strategy.com/debt

- U.S. Securities and Exchange Commission. Administrative Proceeding: Release No. 34-43724, 2000, https://www.sec.gov/enforcement-litigation/administrative-proceedings/34-43724

- Harvard Business School. “MicroStrategy: A Study in Leverage and Strategic Transformation.” Harvard Business School Faculty & Research, https://www.hbs.edu/faculty/Pages/item.aspx?num=61987

- U.S. Securities and Exchange Commission. MicroStrategy Incorporated Form 10-K for Fiscal Year Ended December 31, 2021, https://www.sec.gov/Archives/edgar/data/1050446/000156459022005287/mstr-10k_20211231.htm

- U.S. Securities and Exchange Commission. MicroStrategy Incorporated Form 10-K for Fiscal Year Ended December 31, 2024, https://www.sec.gov/Archives/edgar/data/1050446/000095017025021814/mstr-20241231.htm

Why you can trust 99Bitcoins

Established in 2013, 99Bitcoin’s team members have been crypto experts since Bitcoin’s Early days.

Weekly Research

100k+Monthly readers

Expert contributors

2000+Crypto Projects Reviewed