In This Article

- Top ISO 20022-Compliant Cryptos: Summary

Best ISO 20022 Crypto Coins of 2026

- 1. XRP - ISO Crypto Supporting Cross-Border Payment

- Key Features

- 2. Stellar (XLM) - Focuses on Financial Inclusion & Remittances

- Key Features

- 3. Algorand (ALGO) - ISO 20022 Crypto Supporting CBDCs

- Key Features

- 4. Quant (QNT) - Top ISO 20022 Crypto Focusing on Interoperability

- Key Features

- 5. IOTA - Focuses on IoT payments & Data Integrity

- Key Features

What Is ISO 20022 Crypto?

- ISO 20022 & CBDCs: Are They Related?

- ISO 20022 vs. CBDCs: Comparison Chart

- How ISO 20022 Could Impact the Crypto Industry

- 1. Crypto Can Finally Plug Into Traditional Finance

- 2. Cross-Border Payments Get a Major Upgrade

- 3. Better Data = Better Compliance

- 4. Unlocking Enterprise and Trade Finance Use Cases

- 5. Attracting Institutional Investment

- Conclusion: Best ISO 20022 Cryptocurrencies

ISO 20022 is the messaging standard that banks are upgrading to. It is built for cleaner, more detailed financial data. A handful of crypto projects are built to match it, aiming to work with the same systems used in payments, banking, and compliance.

This guide looks at the best ISO 20022 cryptocurrencies, focusing on the top ISO 20022-compliant coins built for real-world utility, not just hype. If you’re interested in learning more, this ISO 20022 crypto coins list should cover everything you need to know.

Our well-curated ISO 20022 crypto list will help you spot projects that are actually built for integration with banks and financial systems instead of those that use the label as a marketing tactic.

Key Takeaways

- ISO 20022 is changing how banks and payment systems talk to each other, and some crypto projects are building with that in mind.

- These cryptos can carry structured data inside each transaction, which helps with things like audits, compliance, and faster processing.

- Instead of trying to replace banks, they’re built to work with existing systems and fit into real-world financial infrastructure.

- This makes them more useful for cross-border payments, digital currencies, and enterprise tools.

- But just being ISO-ready doesn’t guarantee success, adoption, regulation, and real utility still matter.

- If you’re investing, focus on how the tech is being used, not just whether it checks a box.

Top ISO 20022-Compliant Cryptos: Summary

We’ll break down why ISO 20022 matters, what it has to do with crypto, and which coins are actually built to work with it.

You’ll get a look at the best ISO 20022 coins of 2026, and explain how they fit into things like cross-border payments, CBDCs, and real financial infrastructure.

Along the way, we’ll show you how this all connects to institutional adoption, where to buy these tokens, how to store them, and what risks you need to know before jumping in.

Best ISO 20022 Crypto Coins of 2026

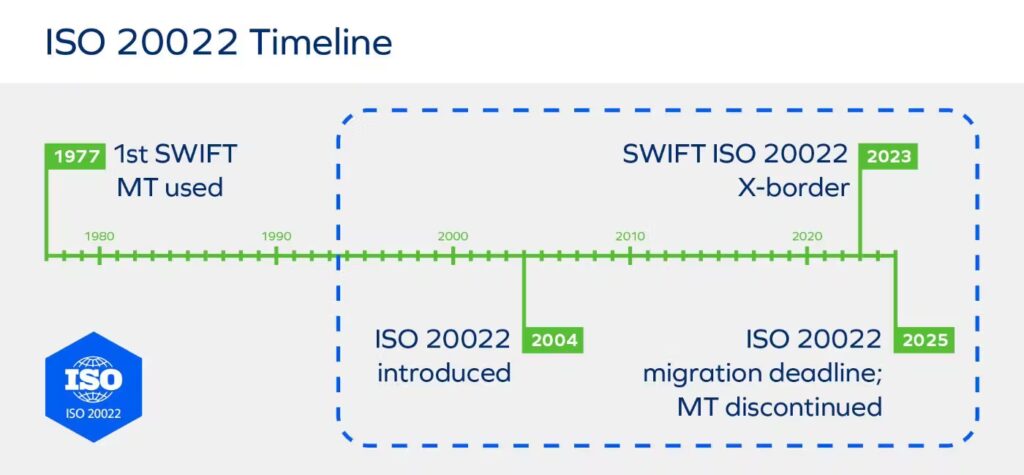

As of mid-2025, global financial systems are moving fast to adopt ISO 20022. The U.S. Federal Reserve’s Fedwire Funds Service transitioned to ISO 20022 messaging on July 14, 2025, and SWIFT’s migration deadlines (including the end of coexistence under CBPR+) approach in November 2025.

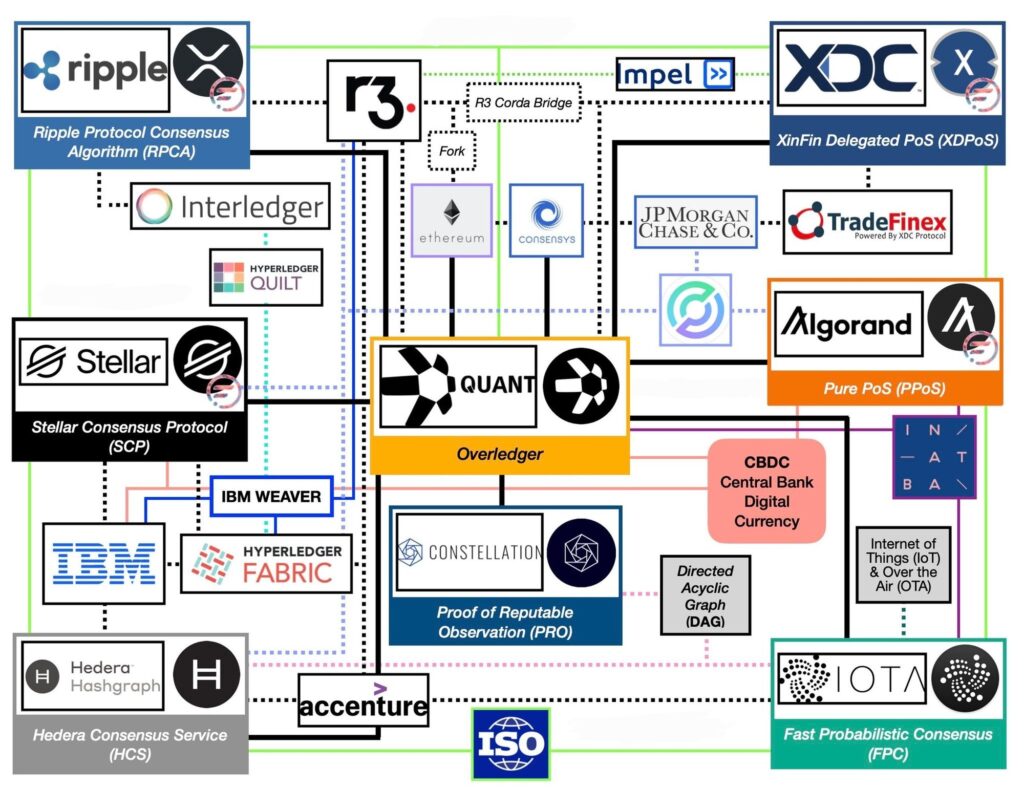

Meanwhile, European authorities-ECB and Deutsche Bundesbank-have formally upgraded ISO 20022 message formats to recognize digital tokens, tokenized financial instruments, and blockchain wallet identifiers. These changes don’t mean all cryptos are officially “certified compliant,” but they do heighten the importance of projects that are already aligned with ISO 20022 standards, such as XRP, Stellar Lumens, Algorand, Quant, XDC Network, IOTA, Hedera, and Cardano.

In this list, we’re covering the top ISO 20022 crypto coins in 2026, the ones with the tech, structure, and use case potential to actually matter in a world where finance is becoming more connected, regulated, and digital.

1. XRP – ISO Crypto Supporting Cross-Border Payment

XRP has carved out a pretty unique role in 2026. It is one of the few digital assets that work well with the ISO 20022 standard, the new global messaging standard that banks are shifting to. Ripple, the company behind the adoption of XRP, joined the ISO 20022 standards body in May 2020, and its RippleNet network was one of the first to support the format.

Even though XRP itself is a cryptocurrency and not a messaging standard, the XRP Ledger’s design matches up well with ISO 20022’s data model. That means financial institutions can use XRP as a bridge currency in compliant cross-border payment setups. It checks the boxes for richer data formatting and compatibility, which are huge for banks moving away from older messaging systems.

The upside for banks using XRP is straightforward: faster transfers, lower fees, and better data baked right into the transactions. Ripple’s On-Demand Liquidity (ODL) taps into XRP to settle international payments without the need for pre-funded bank accounts, which streamlines everything for institutions working inside ISO-compliant systems.

Since XRP is very cheap and fast, settling transactions in 3-5 seconds while costing a fraction of a penny, it’s definitely one of the best ISO 20022 cryptos for cross-border payments.

Key Features

- ISO 20022-Compatible Infrastructure: RippleNet supports ISO 20022 financial messaging, facilitating interoperability with core payment systems and major banks.

- On-Demand Liquidity (ODL): XRP enables real-time liquidity settlement via Ripple’s ODL service without requiring pre-funded accounts in destination countries.

- Fast Settlement & Low Fees: Transactions settle in 3 to 5 seconds at minimal cost, making XRP suitable for both large remittances and small payments.

- Rich Payment Metadata: ISO 20022 compatibility allows XRP transactions to carry enhanced structured data, improving transparency and reconciliation.

- Institutional Partnerships: Ripple has been involved in developing ISO 20022 standards since 2020, and RippleNet is integrated into banks like HSBC and Deutsche Bank.

Curious about where XRP might be headed? Read our XRP Price Prediction for 2026-2030 to understand future market trends.

Pros

-

Seamless Banking Integration: Compatibility with ISO 20022 makes XRP a practical choice for financial institutions looking to modernize their systems.

-

Transaction Efficiency: Fast settlement and ultra-low fees offer major improvements over legacy payment rails.

-

Institutional Credibility: Ripple’s work with ISO bodies and big banks helps legitimize XRP in enterprise finance.

-

Richer Transaction Data: Structured messages support compliance and help reduce fraud by improving traceability.

Cons

-

Not Natively ISO 20022: While RippleNet is ISO compliant, the XRP token itself is not the messaging layer.

-

Regulatory Overhang: Legal uncertainty in some countries still clouds XRP’s adoption.

-

Competitive Landscape: Other projects like Stellar and Algorand are also aligned with ISO 20022, making this a crowded space.

-

Integration Complexity: Bringing XRP into legacy bank infrastructure can be technical and time-consuming.

XRP has positioned itself as a future-facing cross-border payments asset through its close alignment with ISO 20022 and RippleNet’s growing reach in traditional finance.

Its speed, affordability, and integration capabilities give it serious potential as banks overhaul old systems. Still, its success depends on broader adoption, competition, and regulatory questions for those looking to buy Ripple (XRP) or already holding it.

2. Stellar (XLM) – Focuses on Financial Inclusion & Remittances

Stellar (XLM) is another cryptocurrency on our ISO 20022 crypto coins list that is similar in many ways to XRP. Built for cross-border payments and financial inclusion, Stellar was designed with traditional finance in mind.

Thanks to the Stellar Development Foundation’s work, the network aligns with ISO 20022 messaging standards, making it easier for banks and legacy systems to plug in.

What helps XLM stand out is its fast and cheap transaction system. The Stellar Consensus Protocol (SCP) finalizes payments in seconds, often with a fee so tiny it rounds down to zero. Pair that with ISO-friendly metadata, and financial institutions looking to modernize away from SWIFT can see the appeal.

Being ISO 20022-compatible isn’t just a nice-to-have. It means Stellar can carry structured transaction data, like remittance info or compliance details, without skipping a beat. This makes XLM a strong option as a bridge between old-school fiat and decentralized apps (dApps).

With major networks like SWIFT, SEPA, and Fedwire expected to fully adopt ISO 20022 by mid-2025, XLM could benefit from a wave of new integrations. Analysts are also eyeing Stellar’s competitive positioning next to XRP, especially now that messaging standards are a hot topic among institutions.

Stellar (XLM) offers a clean, purpose-built toolset for developers, NGOs, and financial players who want to bridge blockchains and banks. As the ISO upgrade rolls out globally, Stellar is ready to meet it head-on.

Key Features

- ISO 20022 Compatibility: Fully aligns with ISO 20022 messaging, allowing direct integration with legacy banking systems.

- Fast, Low-Cost Transfers: Transactions finalize in 3 to 5 seconds with fees around $0.00001, ideal for micropayments.

- Built-in Decentralized Exchange (DEX): Enables automatic cross-currency conversions using XLM as a bridge asset.

- Anchors & On/Off Ramps: Partners like Circle and MoneyGram provide access to local fiat currency conversions worldwide.

- Humanitarian & Institutional Use Cases: Used by UNHCR for aid distribution and IBM for corporate remittance services.

If you’re holding Stellar (XLM) and see it as a long-term play in digital finance, why don’t you check out our Stellar Lumens ($XLM) price prediction to see where it could be headed?

Pros

-

Inclusivity Focus: Enables access to financial services for unbanked communities via mobile and low-cost transactions.

-

Quick Settlements, Minimal Fees: Achieves near-instant settlement at near-zero cost, outperforming traditional systems.

-

Real-World Adoption: Backed by global corporations and NGOs for use in remittances, payroll, and aid.

-

Structured Payment Data: ISO 20022 compliance enables enhanced transaction metadata, improving transparency and reconciliation.

Cons

-

Adoption Still Growing: While promising, ISO 20022 adoption among banks is still rolling out and not yet universal.

-

Competitive Landscape: Faces competition from other compliant crypto-assets like XRP and ALGO in the ISO space.

-

Technical Integration Needs: Incorporating Stellar into existing financial systems requires development effort and infrastructure updates.

Stellar (XLM) is built from the ground up for financial blockchain interoperability and inclusive payments. Its ISO 20022 alignment, speed, and cost-efficiency put it in a strong position as banks and institutions make the digital leap.

With growing real-world traction and meaningful live use cases, Stellar is technically sound and a grounded blockchain player in the cross-border payment market.

If you’re just getting started, here are 7 ways to buy Stellar Lumens (XLM) instantly in 2026.

3. Algorand (ALGO) – ISO 20022 Crypto Supporting CBDCs

Algorand (ALGO) is a Layer-1 blockchain that doesn’t waste time. With its Pure Proof-of-Stake (PPoS) consensus system, it moves fast, scales well, and settles transactions in seconds. We’re talking up to 10,000 transactions per second, without sacrificing decentralization or security.

Due to its technology, Algorand fits nicely on this list of cryptos compliant with ISO 20022. This gives ALGO an edge for integration with banks, fintech, and even central banks.

Why does this matter? ISO 20022 isn’t just about faster payments. It’s about structured, detailed data that helps reduce errors, smooth out reconciliation, and make compliance less of a headache. Algorand’s setup allows for all that and more, including metadata like KYC info, payment notes, and audit trails.

You’ll also find Algorand discussing central bank digital currencies (CBDCs), asset tokenization, and smart contracts. Its tech isn’t just compatible with ISO standards, it’s built with these high-stakes, high-integrity use cases in mind. That’s why it’s already being adopted by governments and financial institutions, especially in Latin America and Europe.

With ISO migration deadlines wrapping up around late 2025, Algorand seems to be in the right place at the right time.

Key Features

- ISO 20022 Compliant Messaging: Algorand supports structured financial messaging, letting institutions plug in without needing workarounds.

- CBDC-Ready Architecture: Offers dedicated infrastructure and toolkits for central banks to issue digital currency efficiently.

- Pure Proof-of-Stake Consensus: Finalizes transactions in about 2 seconds without energy-hungry mining.

- Post-Quantum Security: Includes FALCON signatures and State Proofs to guard against future quantum threats.

- Enterprise Adoption: Already in use for government platforms, digital asset registries, and payment rails.

You can look deeper at its potential in our Algorand (ALGO) price prediction 2026–2030.

Pros

-

Banking Integration Friendly: Native ISO 20022 support makes it easy for banks to explore blockchain-based solutions.

-

Built for Digital Currency Issuance: Tailored CBDC architecture gives central banks a clear on-ramp.

-

Fast, Scalable, and Secure: High throughput, low latency, and quantum-proof encryption make it robust and future-proof.

-

Proven Track Record: Already powering real-world infrastructure across multiple countries.

Cons

-

ISO 20022 isn’t a Certification: Algorand is compatible with the standard, but there’s no official badge or stamp of approval.

-

Institutional Adoption Lagging: Use cases exist, but large-scale rollouts still depend on regulation.

-

Competitive Pressure: Other ISO-friendly chains like Stellar and XRP target similar audiences.

-

Integration Overhead: Legacy systems don’t update overnight, and adopting Algorand can require custom work and planning.

Algorand is playing the long game. With its mix of speed, resilience, and regulatory readiness, it’s built for the kinds of projects banks, governments, and enterprises care about. From CBDCs to cross-border compliance, ALGO has the correct specs. But before you buy Algorand, know that, like any player in the institutional space, it still needs strong partnerships, regulatory green lights, and continued adoption to stay ahead of the pack.

4. Quant (QNT) – Top ISO 20022 Crypto Focusing on Interoperability

Quant (QNT) is built around the Overledger protocol. It connects the dots between old-school banking systems, permissioned networks, public blockchains, and CBDCs. It’s not just compatible with ISO 20022; it was designed from the ground up to speak that language fluently, which puts it in a solid position as more financial systems move toward standardized messaging.

In April 2025, Quant introduced Quant Flow, which lets institutions automate payments and build compliance-friendly workflows. It’s powered by PayScript®, a custom scripting language that helps companies embed important info like KYC, AML data, remittance notes, and reconciliation tags directly into payments. And it does all this without blinking across complex networks like SWIFT, Fedwire, and Corda.

The QNT token is what makes everything tick. It’s used to access Overledger services, run transactions, and support the best crypto staking system based on actual activity, not speculative hype. With a fixed supply of around 14.6 million, there’s no inflation mechanic inflating your holdings while you sleep. It’s simple: the more real use cases it supports, the more useful the token becomes.

Key Features

- ISO 20022 Alignment: Overledger uses standardized messaging to bridge institutional networks, promoting compliance and uniform communication.

- Cross‑Chain Interoperability: Enables secure transactions and data routing across public and private blockchains, legacy financial systems, and CBDC infrastructures.

- QNT Utility Token: Powers Overledger access, pays service fees, and supports a usage-based staking model tied to real enterprise workflow success.

- Enterprise & Regulatory Focus: Designed for businesses and institutions, Quant offers APIs for CBDC projects (e.g., Project Rosalind with Bank of England) and compliance-ready frameworks.

- Finite Supply & Staking Model: With around 14.6 million QNT minted and no inflation, ongoing staking mechanisms reinforce scarcity and prioritize active usage.

Pros

-

Interoperability Across Systems: Seamlessly connects diverse blockchain and legacy financial systems via a unified protocol layer.

-

ISO 20022 Compliance: Promotes institutional adoption through standardized messaging support.

-

Usage-Based Rewards: Staking tied to real network activity keeps rewards grounded in actual demand.

-

Enterprise-Grade Architecture: Focused on institutional deployment with robust APIs, regulation-aware design, and pilot programs that are already running.

Cons

-

No Native Blockchain Layer: Overledger doesn’t run on its own chain, which could be a dealbreaker for projects looking for an all-in-one ecosystem.

-

Relies on Institutional Uptake: The platform’s growth depends on banks and governments coming on board, and that timeline isn’t exactly predictable.

-

Competitive Field: Projects like XDC, Algorand, and Hedera are also chasing ISO integration, which means Quant isn’t alone in this race.

-

Implementation Complexity: Getting it into production requires deep integration work, especially when dealing with older financial infrastructure.

Quant is taking a more practical route towards finance, building tools that help institutions upgrade what they already have. With ISO 20022 support, programmable workflows, and a role in real-world projects, it’s got a serious shot at playing middleman in tomorrow’s digital finance systems.

But its success depends on how many institutions decide to make the jump. If they do, Quant won’t just be part of the system; it might be the quiet backbone that keeps it all talking. Due to this, Quant fits neatly into our roundup of the top ISO 20022 crypto tokens.

5. IOTA – Focuses on IoT payments & Data Integrity

IOTA (MIOTA) differs from most cryptocurrencies, especially when it was launched (July 2016). Instead of chaining blocks like everyone else, it runs on a Directed Acyclic Graph (DAG) called the Tangle. It sounds complex, but the takeaway is simple: It allows devices to send value and data without paying fees, which is a huge deal for microtransactions in IoT environments.

Since IOTA is feeless, it is a good option as an ISO 20022 crypto, giving it the potential to work alongside financial institutions and central banks.

Where IOTA gets interesting is how it handles data. The Tangle doesn’t just move coins; it can embed structured financial messages directly into transactions. That means things like remittance info or KYC metadata can flow alongside payments, making IOTA a good fit for systems that rely on clear, regulated messaging like SWIFT or CBDC networks.

Its biggest selling point? Zero fees. In an industry where every transaction usually comes with a price tag, IOTA’s model makes it ideal for situations where devices need to talk constantly without racking up a bill. From smart factories to real-time logistics, this feeless framework fits right into use cases that need high-frequency data and value exchange.

IOTA may not look like the usual ISO-aligned players such as XRP or Stellar, but in terms of raw utility for the machine economy, it brings something different.

Key Features

- ISO 20022 Alignment: Designed to support structured financial messaging standards, aiding future integration with banking and payment networks.

- Feeless Microtransactions: Enables instantaneous, cost-free transactions ideal for IoT devices communicating or transacting value.

- Scalable DAG Architecture (Tangle): Improves transaction throughput as usage grows, no mining or heavy network fees required.

- Data Integrity Messaging: Capable of securely transferring both value and data packets, enabling immutable machine-to-machine communication.

- Post-Migration Decentralization: Plans to remove its centralized coordinator via Coordicide, improving resilience and governance.

Pros

-

ISO 20022 Compatibility: Paves the way for secure, compliant messaging between IoT networks and traditional finance infrastructures.

-

Micropayment Efficiency: Feeless design supports numerous low-value transactions essential for IoT ecosystems.

-

High Scalability: DAG-based protocol enhances performance with network growth, no mining bottlenecks.

-

Strong Data Security: Enables secure, immutable data transfers between connected devices for audit and traceability.

Cons

-

Ongoing Decentralization: It currently relies on a coordinator node; a fully decentralized architecture (Coordicide) is still being rolled out.

-

Complex Consensus Resilience: Research indicates IOTA’s consensus mechanisms may struggle under certain network conditions.

-

Adoption Constraints: Limited real-world deployment in IoT finance compared to more established blockchain ecosystems.

-

Integration Challenges: Linking DAG and ISO frameworks with legacy finance systems requires complex development and coordination.

IOTA brings a fresh perspective to the blockchain space, focusing on feeless microtransactions and IoT-first architecture. Its readiness for ISO 20022 gives it a bridge to formal financial messaging without sacrificing its uniqueness.

The technical potential is there, but long-term success will depend on how well it decentralizes and integrates with the regulated world. If it pulls that off, IOTA could be the quiet enabler behind how machines handle money and data in the years ahead. If many users adopt the project or buy IOTA, it could become one of the most popular cryptocurrencies used in ISO 20022 payments.

What Is ISO 20022 Crypto?

ISO 20022 crypto refers to digital assets that are built to “speak the language” of the financial world. And by that, we mean they’re compatible with the ISO 20022 standard, a global messaging format used by banks and financial institutions to send electronic data in a clear, structured way.

Right now, many traditional financial systems rely on older, clunky message formats that were never designed to handle today’s fast, complex money movement. ISO 20022 changes that. It’s like upgrading from a flip phone to a smartphone. It allows for richer, more detailed financial information, which is a big deal for everything from cross-border payments to trade finance and even regulatory compliance.

Now, cryptos that are ISO 20022 compliant are the ones positioning themselves to work directly with this next-gen financial messaging system. These tokens are designed to plug into existing financial infrastructure, offering the kind of seamless integration that banks and financial entities need if they’re going to adopt blockchain tech.

In other words, ISO 20022 crypto is the bridge between blockchain networks and the traditional finance system.

- XRP (Ripple): Used for efficient cross-border transactions, especially by banks and international payment systems.

- XLM (Stellar): Known for low-fee remittances and working with external financial systems like Visa and MoneyGram.

- QNT (Quant): Its Overledger connects different financial systems, including banks and multiple blockchains.

- XDC (XDC Network): Built for trade finance, supply chain finance, and electronic data interchange.

- ALGO, HBAR, MIOTA: Fast, scalable platforms focused on data exchange and secure and scalable transactions.

Some of the best ISO 20022-compliant cryptocurrencies for banks, like XRP, XLM, and XDC, aren’t officially certified, but they’re built according to ISO 20022 standards. Their networks can handle structured data and metadata, which makes them a good fit for future financial systems that move toward ISO 20022.

For example, the RippleNet Payment Object includes fields (like ChrgBr) that come directly from ISO 20022 schemas. Also, as Omni Network co-founder Austin King points out:

“What did $XRP prioritize before any other crypto and processes over $434,000,000,000 each day? ISO 20022 —few people understand how important this is.”

These cryptocurrencies won’t be replacing SWIFT (just yet), but they’re built with compatibility in mind. When looking at ISO 20022 vs SWIFT for crypto payments, ISO 20022 stands out because it allows more detailed and flexible messaging. That makes it easier to work with modern tech like blockchain, compared to SWIFT’s older, more limited format.

ISO 20022 & CBDCs: Are They Related?

ISO 20022 and CBDCs are like peanut butter and jelly. They’re different but made to work together.

ISO 20022 is a global standard for formatting and sending financial messages between banks, clearinghouses, and other financial entities. It’s all about consistency and clarity in financial communications. Think of it like a universal translator for money.

CBDCs, on the other hand, are a completely digital version of a country’s currency. But if a digital dollar or digital euro is going to work with the world’s banking infrastructure, it needs to follow the same messaging rules as everything else. That’s where ISO 20022 comes in.

When a CBDC is ISO 20022 compliant, it can smoothly connect with other systems, including older banks, newer blockchain networks, and international payment systems. It’s what makes seamless integration possible between new money tech and the traditional finance system.

CBDCs don’t have to use ISO 20022, but they do need it if they want to be useful on a global scale, especially for cross-border transactions, regulatory compliance, and secure record-keeping.

ISO 20022 vs. CBDCs: Comparison Chart

| Feature | ISO 20022 | Central Bank Digital Currency (CBDC) |

|---|---|---|

| Definition | A global standard for sending financial messages | A digital form of fiat currency issued by a central bank |

| Main Purpose | Standardizes financial messaging capabilities across systems | Enables digital money that works in the real world |

| Use Cases | Used by banks, networks, and payment systems | Used by individuals, businesses, and governments |

| Tech Format | XML-based electronic data exchange | Blockchain or non-blockchain digital payment protocol |

| Global Adoption | 70+ countries are already switching over | 100+ countries are exploring or piloting CBDCs |

| Need for Each Other | ISO helps CBDCs connect to existing financial infrastructure | CBDCs benefit from ISO to communicate effectively |

| Supports Metadata? | Yes, for AML, KYC, and audit purposes | Yes, varies by country’s design and regulations |

| Examples | RippleNet, SWIFT MX, and ISO-ready crypto | e-CNY, Digital Euro, eNaira, and others |

This comparison makes it pretty clear that ISO 20022 and CBDCs may be different tools, but they’re meant to work together. The ISO 20022 crypto standard gives CBDCs the structure they need to connect with everything from traditional financial systems and banking systems to modern blockchain networks and global payment settlement infrastructure.

Without this shared language, CBDCs would be stuck trying to talk to legacy tech using a brand-new dialect, and that just doesn’t work in real-world finance. ISO 20022 solves that by enabling seamless integration across all types of financial institutions, making electronic data exchange smoother, faster, and more accurate.

It also lowers transaction costs, which is important for everything from cross-border payments to global trade. Regulators love it because it supports better tracking, reporting, and financial information sharing. Since CBDCs will interact with all kinds of existing financial infrastructure, being ISO-ready has already gained significant importance.

In short, ISO 20022 is like the connector cable between old-school finance and the future of money. If a CBDC wants to work across borders, plug into the traditional finance system, and play nice with private cryptos, this global standard is how it speaks the right language.

Looking for coins with the highest return potential?

Learn from our expert-picked list of 12 coins with high returns for the best August forecast.

How ISO 20022 Could Impact the Crypto Industry

The ISO 20022 standard is changing how the financial sector communicates, and crypto is finally being invited to the table. Here’s how this could change everything for the crypto space:

1. Crypto Can Finally Plug Into Traditional Finance

One of the biggest issues with crypto has always been its lack of connection to mainstream finance. By becoming ISO 20022 compliant, certain tokens like XRP, XDC, and QNT can now interface with traditional financial institutions, banking infrastructure, and other financial entities, without needing to completely replace them.

2. Cross-Border Payments Get a Major Upgrade

Tokens aligned with ISO 20022 can support faster, cheaper, and more transparent cross-border payments. This is huge for remittances, foreign exchange, and international payment systems. Instead of days of waiting and high transaction fees, we’re talking near-instant transfers with embedded metadata to track everything in real-time.

3. Better Data = Better Compliance

ISO 20022 allows for detailed, structured messaging, which includes regulatory and compliance data. This is something that’s been missing in a lot of blockchain networks. Now, crypto projects that follow this standard can actually meet the expectations of the financial industry, which is essential for audits, AML, and real-time monitoring.

4. Unlocking Enterprise and Trade Finance Use Cases

The XDC Network is already diving deep into areas like trade finance and supply chain finance, which rely on systems that need lots of paperwork, tracking, and structured data. ISO 20022 enables electronic data interchange that can automate a lot of that, cutting costs and increasing trust.

5. Attracting Institutional Investment

For years, institutions have hesitated to touch crypto. Too risky, too hard to integrate, too vague. But ISO 20022-compliant assets change the narrative. They offer the kind of structure and seamless communication that institutions expect from other financial systems. That’s a game-changer for institutional investment and long-term adoption.

For cryptocurrency to truly scale and become part of mainstream finance, it has to learn to communicate with the financial systems already in place. ISO 20022 makes this possible.

This standard gives crypto projects the tools to connect with the traditional financial sector through structured data exchange, secure and scalable transactions, and seamless integration with external financial systems. It bridges the gap between cutting-edge tech and the financial messaging capabilities banks and institutions rely on daily.

Tokens like XRP, XDC, QNT, and others are leading the way by preparing for that future. Whether cross-border payments, regulatory compliance, or trade finance, ISO 20022-compliant positions them for real-world usage in the financial industry.

Crypto isn’t just a disruptor anymore; it’s becoming part of the system. ISO 20022 is the roadmap that finally makes facilitating smoother communication across all types of financial entities possible.

How to Choose the Right ISO 20022 Crypto?

Not all ISO 20022 cryptos are the same. Some are genuinely trying to build bridges between crypto and real-world finance, but, as with the crypto market, there will be projects that simply want to capitalize on the popularity surrounding the narrative.

Here’s some advice to help you separate the promising projects from the money grabs and potential rug pulls.

1. What’s it actually for?

Don’t just ask what the token does, ask who it helps. Is it solving real problems like sending money across borders faster, assisting banks to connect with blockchain, or making global payments more transparent? Or is it just claiming to be “ISO 20022 ready” with no clear use?

If there’s no real-world application or clear audience, skip it.

2. Is anyone important using it?

Look at partnerships. If a project is being tested or used by banks, payment networks, or fintech companies, that’s a strong sign. These institutions don’t mess around; they want reliability, regulation, and compatibility. If a crypto is in their systems or pilot programs, it’s worth paying attention to.

3. Does it actually work with legacy finance?

One of ISO 20022 crypto’s biggest promises is that it can plug into existing financial systems without breaking everything. So, you want projects that are built with interoperability in mind, meaning they can “talk” to both modern blockchain networks and the old-school banking world.

That includes message formatting, compliance data, and audit trails.

4. Is it fast, cheap, and scalable?

It’s 2026. If a token still charges crazy fees or takes forever to process a transaction, it’s not built for serious finance. You want something that can handle a high volume of transactions quickly, without massive overhead, especially if it’s meant to help move money across borders or power enterprise systems.

5. Who’s behind it?

The team and their track record matter. Are they ex-bankers and engineers who’ve worked in fintech or finance before? Or are they a group of anonymous Twitter handles promising a moon mission?

Also, check if the project has a real roadmap or just a hype-filled whitepaper. You want direction, not dreams.

6. Are institutions or governments taking it seriously?

This is where things get interesting. If big financial players, governments, or infrastructure providers are even testing the token, they see potential. That kind of backing tells you the project isn’t just built for retail, it’s aiming for the core of the financial system.

Choose projects that build real bridges, not just throw buzzwords around, trying to attract investors who don’t know any better.

If a token can genuinely integrate with crypto and traditional finance and has the adoption, vision, and performance to match, you’re probably on the right track.

Where to Buy ISO 20022-Compliant Cryptos?

Want to buy the Best ISO 20022 coins but not sure where to look? This quick list shows you which exchanges offer them: no fluff, just the platforms that let you get tokens like XRP, XLM, and XDC.

Best Wallet

Best Wallet is a non-custodial wallet in a multi-chain mobile app that doesn’t overcomplicate things. It gives you one clean place to buy, swap, stake, and track crypto across 60-plus blockchains without needing five different apps or a computer science degree.

It’s tightly integrated with Onramper and a bunch of the best decentralized exchange (DEX) aggregators under the hood, so the backend handles the heavy lifting. At the same time, you focus on managing your assets. What makes it especially interesting is its tilt toward ISO 20022‑friendly tokens like Stellar, Algorand, and Cardano, making it useful for anyone leaning into the regulated side of crypto.

Key Features

- Built‑in Buy & Swap: Offers fiat on‑ramps via Onramper and DEX swapping with the best rates across 200+ liquidity sources.

- Multi‑Chain Support: Enables management of assets across 60+ networks from a single app, no multiple wallets required.

- Self‑Custody Security: Private keys are stored locally with biometric, PIN, and two‑factor protection, backed by Fireblocks technology.

- Staking Aggregator: Users can stake tokens within the app using automated yield optimization across multiple networks.

- Launchpad & Airdrops: Access presale token launches and earn $BEST tokens for early participation and app usage.

Pros and Cons

Pros

- Versatile All‑In‑One Tool: Combines buying, swapping, staking, and portfolio tracking across multiple ISO‑compliant networks.

- No KYC Required for Core Features: Non‑custodial access without identity verification, ideal for privacy‑focused users.

- Institution‑Grade Security: Integrates Fireblocks, biometrics, encrypted key storage, and real‑time monitoring.

- Rich Crypto Ecosystem: Supports over 60 chains, token launches, staking, and high liquidity swaps.

Cons

- Mobile‑Only Access: Lacks a desktop or browser extension, which may limit advanced traders.

- Emerging Reputation: As a newer product, it has some critical reviews and a limited long-term trust history.

- Reliance on External Aggregators: Swap pricing depends on third-party exchanges, which may vary in reliability.

- No Official ISO Certification: Supports ISO 20022‑aligned tokens, but the app itself is not ISO‑certified.

Best Wallet gives off practical energy; it’s not flashy, but it gets the job done like a top web3 wallet. If you’re looking for a mobile-first wallet that plays well with ISO‑aligned crypto, lets you buy and stake without jumping through hoops, and keeps your keys in your own hands, this one’s worth a look.

It’s still building its track record, and you’ll need to be cool with using your phone for everything, but for users who value control and simplicity, it brings a lot to the table.

Check our Best Wallet Review for more details.

Binance

Binance is about as close to a household name as you get in crypto. Since launching in 2017, it’s grown into one of the most powerful exchanges globally, offering pretty much every tool a trader or investor could ask for. But what makes Binance interesting here is its attention to ISO 20022-compliant tokens.

You’re not just getting access to these assets, you’re getting them through an exchange that actually understands what institutional-grade infrastructure should look like. Whether you’re a seasoned pro or a curious newcomer digging into regulated crypto, Binance doesn’t leave you short on options.

Key Features

- Wide ISO 20022 Token Support: Lists all major compliant assets, including XRP, ADA, ALGO, XLM, QNT, HBAR, IOTA, XDC, enabling diversified access in one ecosystem.

- Deep Liquidity Pools: Offers instant transaction execution with minimal slippage for compliant tokens across fiat and crypto pairs.

- Fiat On‑Ramp Options: Multiple fiat gateways, including credit/debit cards, bank transfers, and P2P, streamline access to ISO assets.

- Advanced Trading Tools: Integrated charting, varied order types (limit, stop-limit), and portfolio management aligned with institutional standards.

- Security & Compliance Layers: Utilizes cold storage, 2FA, and proof-of-reserves audits alongside a global compliance framework.

Pros and Cons

Pros

- Broad Access to ISO Assets: Centralized access to the full suite of compliant tokens under one unified exchange.

- High Liquidity & Speed: Institutional-level volume supports rapid, low-cost transactions across multiple fiat and crypto pairs.

- Robust Enterprise Tools: Advanced functionality makes it suitable for institutional trading strategies and professional portfolio management.

- Comprehensive On‑Ramp Infrastructure: Enables fiat-to-ISO crypto transitions via reliable card, bank, and P2P channels.

Cons

- Regulatory Pressure: Faces ongoing scrutiny and compliance challenges in jurisdictions like the UK and US.

- Potential Over-Reliance: Heavy dependence on Binance’s infrastructure could pose custodial or risk concerns.

- Not ISO Certified Itself: The exchange supports ISO‑compliant tokens, but the platform isn’t ISO‑certified.

- Complexity for Beginners: Feature-rich environment may feel overwhelming to users unfamiliar with ISO or institutional workflows.

Binance is many things, fast, liquid, massive, but most importantly, it’s one of the easiest places to get your hands on a wide range of ISO 20022-aligned tokens. It’s not a perfect fit for everyone, especially if you’re brand new or live in a region where regulation is tightening. Still, if you’re serious about managing compliant crypto assets with room to grow, Binance is tough to ignore.

Look into our separate Binance review for more.

KuCoin

KuCoin, launched in 2017 and now operating out of Seychelles, has built a name for itself by doing a little bit of everything, and doing it well. Whether you’re into spot trading, margin, futures, or just exploring ISO‑aligned tokens, KuCoin gives you a lot to play with.

It recently received an ISO 27001:2022 certification, which isn’t the same as ISO 20022 but shows that it takes data security seriously. The ISO 20022 front offers a strong lineup: XRP, XLM, QNT, ALGO, IOTA, and more. If you want to stack compliant tokens, KuCoin gives you a range without too much noise.

Key Features

- ISO 20022-Compatible Asset Offering: Has a solid list of aligned assets like XRP, ADA, ALGO, XLM, QNT, HBAR, IOTA, and XDC.

- Strong Security Posture: ISO 27001:2022 certified, which means they’ve tightened things up on the security and operational front.

- Comprehensive Trading Instruments: Spot, futures, margin, P2P, OTC, and even leveraged tokens if that’s your lane.

- Multi-Fiat On‑Ramp Support: Depending on your region, buy crypto with cards, bank transfers, or P2P.

- Global User Support & Liquidity: High-volume markets and round-the-clock help make jumping in at any time easy.

Pros and Cons

Pros

- Wide Compliance Asset Access: Easy access to a bunch of ISO-aligned tokens in one place.

- Enhanced Security Measures: The ISO 27001 badge gives confidence that they’ve done the work behind the scenes.

- Versatile Trading Options: Whether you’re casual or running bots, there’s a format for you.

- Smooth Fiat Integration: Lots of ways to get your money in and out without too much hassle.

Cons

- Not for Everyone: Users in the U.S., U.K., and Canada are blocked, so check availability first.

- ISO 20022 Support, Not Certification: The tokens are aligned, but KuCoin isn’t ISO 20022 certified by itself.

- Can Feel a Bit Complex: The interface isn’t the most beginner-friendly if you’re starting out.

- Relies on Third Parties: Some payment channels and on-ramps go through external providers, which could lead to occasional hiccups.

KuCoin feels like the exchange you graduate to when you want more options but don’t want to dive into overly complex institutional tools. It covers a lot of ground, especially for ISO 20022 token hunters, and balances flexibility with solid security.

Just be mindful of the regions it doesn’t serve, and expect a bit of a learning curve if you’re new. Once you’re in, a feature-rich environment gives you room to experiment without feeling bloated.

Learn more about this exchange in our KuCoin review.

MEXC

MEXC was launched in 2018 and has since grown into a major cryptocurrency exchange, serving millions of users worldwide. It offers just about every trading option: spot, margin, futures, leveraged ETFs, and even NFT indexes.

What makes it especially interesting in 2026 is that it offers access to all eight ISO 20022-friendly tokens: XRP, XLM, ALGO, MIOTA, HBAR, QNT, XDC, and ADA.

If you’re looking to build a portfolio around compliance and future-ready infrastructure, this is one of the few places that ticks all the boxes. On the security side, it’s not just talk, MEXC has ISO 27001 certification and runs frequent audits and bug bounty programs to keep things tight.

Key Features

- ISO 20022 Token Support: Gives access to all eight of the top ISO-compliant tokens in one spot.

- ISO 27001 Security Certification: The platform takes its security and operational processes seriously.

- Wide Product Range: Lets you trade everything from basic spot to futures and savings, plus NFTs and leveraged ETFs.

- Tiered KYC Model: You can start trading with limited access, then unlock more features through verification.

- Global Fiat On‑Ramps: Supports multiple ways to deposit, including cards, bank transfers, OTC, and peer-to-peer options.

Pros and Cons

Pros

- Comprehensive ISO Asset Access: It makes accessing a full spread of compliant tokens easy.

- Strong Security Credentials: ISO certification, audits, and bug bounties help build user trust.

- Feature-Rich Trading Environment: Covers everything from regular trades to more advanced investment tools.

- Flexible KYC & On‑Ramp Options: Let users ease in before going through the full ID process.

Cons

- U.S. Market Exclusion: Users in the U.S. are out of luck due to regulatory limitations.

- Platform Complexity: The sheer number of features might be a bit much for newer traders.

- Partial KYC Access: Unverified users face strict withdrawal limits and fewer features.

- Third‑Party Fiat Dependencies: Relies on external providers for fiat, which can add friction depending on location.

MEXC is one of the more complete exchanges for anyone focused on ISO 20022-aligned crypto. The platform has the right tokens, plenty of tools for active traders, and solid security practices.

It’s not the simplest exchange to jump into, and U.S. users are left out entirely, but for those who can access it and want full control over a compliance-friendly portfolio, MEXC is worth considering.

Look at our dedicated MEXC review to know more.

OKX

OKX has been around in some form since 2013, originally under the OKEx name. It rebranded in 2022 and now operates globally from San Jose with thousands of employees spread across multiple offices.

What sets OKX apart is its blend of a heavy-duty trading engine and security stack with a surprisingly polished Web3 setup.

The built-in wallet talks to over 130 blockchains, and the platform holds licenses in all the key jurisdictions, the U.S., EU, Singapore, Australia, UAE, and others. With certifications like SOC 1, SOC 2 Type II, and ISO 27001, plus monthly Proof-of-Reserves audits, it shows serious follow-through on keeping user assets in check.

Key Features

- ISO 20022 Asset Support: Supports a full range of ISO-aligned cryptos, including XRP, XLM, ALGO, QNT, ADA, HBAR, MIOTA, and XDC

- Regulatory Licensing: Actively licensed across major regions including the U.S., EU, Singapore, Australia, and the UAE

- Institutional‑Grade Infrastructure: Offers advanced trading tools, high-speed APIs, futures and options markets, OTC desks, and cross-chain services

- Security & Compliance Certifications: Carries ISO 27001 and SOC 2 credentials, plus monthly third-party Proof-of-Reserves using zk-STARK

- Integrated Web3 Wallet: Lets you store and move assets across chains, connect to dApps, manage NFTs, and tap into decentralized protocols

Pros and Cons

Pros

- Institutional-Grade Compliance: Licensed and certified across major financial regions, giving confidence to bigger players

- Broad ISO 20022 Token Suite: Covers all the major ISO-compliant assets under one roof

- Advanced Trading & Liquidity: Supports complex trading strategies with deep liquidity, fast execution, and tight spreads

- Proof-of-Reserves Transparency: Audited monthly to show users their assets are fully backed

- Comprehensive Web3 Features: Wallet is built-in and covers multi-chain access, NFT support, and cross-chain swaps

Cons

- Complexity for Casual Users: With this many tools and options, beginners may need time to find their footing

- KYC Required for Full Access: You’ll need to verify your identity to use key features like fiat deposits or withdrawals

- Regional Rollouts Vary: Not every feature is available everywhere yet; it depends on your country’s regulations

OKX packs a lot into one platform. It’s designed for people who want a serious setup with tight compliance, fast performance, and tools beyond basic trading. The integrated Web3 wallet and broad ISO token support give it an edge for users looking to move between traditional finance and blockchain ecosystems.

But with that power comes a bit of complexity, and it might not be the easiest entry point for casual users. Still, OKX checks most of the boxes for those who want compliant assets with transparency and control.

Head to our OKX review for 2026 for everything else.

How to Buy ISO 20022 Cryptos: Step-by-Step Guide

Buying ISO 20022-compliant crypto tokens isn’t complicated, but you need the right tools. For this example, we’ll use Best Wallet, a self-custody smart wallet that works with decentralized and centralized exchanges. You stay in control the whole time, without relying on third parties to hold your crypto.

-

Download Best Wallet

Go to bestwallet.com and download the app for iOS or Android. You can also create a browser wallet. Pick whatever’s more convenient.

-

Create Your Wallet

Follow the setup instructions. You’ll get a recovery phrase. Write it down. Don’t screenshot it. Don’t store it in your email. This phrase is your lifeline.

-

Secure Everything

Turn on biometric login or PIN, and make sure your recovery phrase is backed up properly. No one’s coming to save you if you lose it.

-

Add Funds to Your Wallet

Use a card or bank transfer to buy crypto directly inside the app, or move funds over from another exchange like Binance or Coinbase. Start with ETH or USDT for flexibility.

-

Find and Buy ISO 20022 Tokens

Use the Trade tab. You can connect to centralized exchanges or DEXs inside Best Wallet. Search for tokens like XRP, XLM, XDC, ALGO, or QNT. Swap using a supported pair like USDT/XDC or ETH/XLM.

-

Check the Token Format

Some tokens come in different network versions. Make sure you’re buying the right one. If you’re not sure, read the token’s official site or look it up on CoinGecko.

-

Store and Watch Your Tokens

Once the trade’s complete, your tokens show up in your wallet. You can track your portfolio, set price alerts, and stake certain tokens if supported. Withdraw or swap whenever you want.

That’s it. You now own an ISO 20022 crypto, and it’s sitting safely in a wallet you control. No waiting periods, locked funds, or asking a support team for permission.

Just check the token’s fundamentals before buying and stay on top of any network support or exchange access changes.

Benefits & Risks of Investing in ISO 20022 Crypto Coins

Before putting money into ISO 20022 tokens, it’s worth stepping back and looking at what you’re actually getting into, the upsides, and the stuff that could trip you up.

Benefits

- Stronger Reputation: ISO 20022 tokens are often seen as more credible because they follow standards already used by banks.

- Useful Data: The messaging format allows for more detailed transaction info, which could help with tracking usage and activity.

- Easier Integration: These tokens are designed to fit into existing banking and payment systems, which may increase their long-term utility.

- Compliance-Ready: Some ISO-aligned tokens are structured to handle audits and regulatory requirements more easily than others.

- Institutional Interest: A few projects (like XRP and XLM) already have partnerships with banks or payment providers, giving them real-world traction.

Risks

- Still Volatile: Prices can move fast and unpredictably, even with bank partnerships or real-world use cases.

- Not Legally Protected: ISO 20022 alignment doesn’t mean regulators will leave them alone; XRP’s legal battle is proof.

- Slow Adoption: Banks and governments don’t move quickly. A token might be ready on paper but unused for years.

- Centralized Control: Some projects rely on small teams or companies, which can limit transparency and increase risk.

- Limited Availability: Certain ISO 20022 tokens aren’t listed on major exchanges, which can make them harder to buy or sell.

There’s upside here, but it’s not without friction. If you’re betting on ISO 20022 tokens, do it with a clear head and a long-term view.

Top Wallets for Storing ISO 20022 Tokens

If you’re holding ISO 20022 coins, such as XRP, XLM, or XDC, you’ll want a wallet that’s secure, easy to use, and supports these assets. Here are some of the top options to consider:

- Best Wallet: A beginner-friendly wallet app (with a built-in DEX) that lets you buy, store, swap, and sell ISO 20022 tokens all in one place.

- Zengo: A mobile wallet with no seed phrase and strong security, making it a solid choice for storing coins like XRP and XLM. Visit the detailed Zengo review.

- Ledger Flex: A touchscreen hardware wallet that keeps your crypto offline and supports ISO-aligned tokens through third-party apps. Learn more at our Ledger Stax vs Flex review.

- Trezor Safe 5: A secure hardware wallet that works with coins like XRP, XLM, ADA, and XDC, and connects with both Trezor Suite and other apps. Check the Trezor Safe 5 review.

These wallets cater to a range of needs, from mobile convenience to offline storage. Pick the one that fits your setup and the ISO 20022 tokens you want to hold safely.

Conclusion: Best ISO 20022 Cryptocurrencies

ISO 20022 crypto projects are gaining attention for their ability to integrate seamlessly with existing global banking and payment systems. Unlike speculative tokens built primarily for trading hype, ISO 20022-compliant cryptocurrencies are designed for real-world utility, directly connecting with institutions, cross-border payment networks, and digital finance infrastructure.

However, ISO compliance alone doesn’t guarantee success. Smart investors should evaluate each project’s real integrations, blockchain infrastructure, and level of institutional adoption. The ISO 20022 standard provides the framework, but sustained usage and partnerships will define which tokens truly support the future of financial messaging and interoperability.

For those seeking long-term, utility-driven crypto investments, ISO 20022 coins offer one of the clearest bridges between traditional finance and blockchain innovation. Focus on the projects actively building enterprise-grade solutions and forging partnerships with banks, fintechs, and payment processors.

See also:

FAQs

Why is ISO 20022 important for cryptocurrencies?

It gives crypto projects a way to connect with the systems banks and financial institutions already use. That means smoother integration for things like payments, compliance, and financial data sharing.

Is Hedera fully ISO 20022 compliant?

Yes. Hedera is ISO 20022-compliant and supports structured financial messaging. It’s also part of the ISO 20022 standards body, making it one of the few crypto networks built with full alignment in mind.

What makes a crypto ISO 20022-compliant?

A crypto is considered ISO 20022-compliant if its network can handle structured messaging that matches the ISO 20022 format. This includes support for metadata, payment details, and financial information used by banks.

Will ISO 20022 cryptos replace SWIFT?

No. These cryptocurrencies are designed to work alongside systems like SWIFT and not replace them. ISO 20022 is a messaging format, not a network or payment rail.

Are ISO 20022 coins good investments?

ISO 20022 coins have potential because of their focus on real-world use, but they’re still subject to the same risks as the rest of the crypto market. Compliance alone doesn’t make them safe or guaranteed to grow.

Is ISO 20022 only used by banks?

No, while banks use it heavily, ISO 20022 is also used by payment processors, financial institutions, fintech platforms, and even blockchain networks that want to ensure compatibility with global financial messaging standards.

References:

- ISO 20022. “ISO 20022.” ISO 20022, https://www.iso20022.org/.

- Stellar Development Foundation. “Stellar Consensus Protocol.” Stellar, https://stellar.org/learn/stellar-consensus-protocol.

- MEXC. “On-Demand Liquidity (ODL).” MEXC Blog, https://blog.mexc.com/glossary/on-demand-liquidity-odl.

- Federal Reserve Financial Services. “ISO 20022 Implementation Center.” FRB Services, https://www.frbservices.org/resources/financial-services/wires/iso-20022-implementation-center.

- Algorand. “Pure Proof-of-Stake.” Algorand, https://algorand.co/technology/pure-proof-of-stake.

- The Financial Technology Report. “Quant Introduces Quant Flow to Advance Programmable Money in Finance Sector.” The Financial Technology Report, https://thefinancialtechnologyreport.com/quant-introduces-quant-flow-to-advance-programmable-money-in-finance-sector/.

- IBM. “What Is a Directed Acyclic Graph (DAG)?” IBM Think, https://www.ibm.com/think/topics/directed-acyclic-graph.

- Investopedia. “Tangle (Cryptocurrency).” Investopedia, https://www.investopedia.com/terms/t/tangle-cryptocurrency.asp.

- Ripple. “Standard RippleNet Payment Object.” Ripple Docs, https://docs.ripple.com/payments-odl/api-docs/ripplenet/resources/standard-ripplenet-payment-object/.

Why you can trust 99Bitcoins

Established in 2013, 99Bitcoin’s team members have been crypto experts since Bitcoin’s Early days.

Weekly Research

100k+Monthly readers

Expert contributors

2000+Crypto Projects Reviewed