In This Article

With interest rates being as high as they are, simply holding USDC or USDT and earning yield on Coinbase or Aave for 5-12% has been a popular strategy over the past few years. However, a bill called the Clarity Act could change that setup, and crypto holders need to prepare and act soon.

Specifically, a provision in the clarity act crypto bill would block centralized platforms from paying you interest just for holding a stablecoin. This guide covers what the Digital Asset Market Clarity Act actually says, why the stablecoin yield question matters to you personally, and what you can do right now.

What Is the Clarity Act? A Plain-English Definition

The Clarity Act (officially the Digital Asset Market Clarity Act of 2025, H.R. 3633) sorts every digital asset into one of three buckets: securities, digital commodities, or stablecoins. Then it assigns the SEC or CFTC as the clear regulator for each bucket.

For years, crypto lived in a gray zone, with our friend Gary Gensler, head of the SEC, regulating by enforcement and issuing Wells Notices to anything that even rhymed with crypto.

In the early years of crypto, both the SEC and CFTC claimed jurisdiction over the digital asset space in a sort of turf war between agencies. Builders, exchanges, and retail users had no clear answer on which rules actually applied. The Clarity Act draws those lines for the first time. Fortunately, these dark days are behind us, thanks to a friendlier regulatory landscape in the United States.

Here’s what the bill does in plain terms:

- Classifies every digital asset into one of three regulated categories (securities, digital commodities, or stablecoins).

- Assigns the SEC or CFTC as the clear regulator for each category.

- Sets rules for stablecoin issuers and the platforms (exchanges, DeFi protocols, custodians) that offer them.

Want a refresher on stablecoins? See our guide on what is a stablecoin?

GENIUS Act vs. Clarity Act: What Is the Difference?

You’ve probably seen both names in headlines. They’re two separate bills, and only one has become law. The Crypto Clarity Act is the broader market structure bill. The GENIUS Act is the narrower stablecoin issuer law that passed first.

GENIUS Act vs. Clarity Act: Key Differences at a Glance

| GENIUS Act | Clarity Act | |

| Status | Signed into law (July 18, 2025) | Passed House; Senate stalled |

| What it covers | Stablecoin issuers only | All digital assets (full market) |

| Who it targets | Circle, Tether (issuers) | Exchanges, DeFi protocols, platforms |

| Yields/Rewards | Bans issuer-paid yield | Proposes to ban platform-paid yield (Section 404) |

| Regulators assigned | OCC, Treasury, FDIC | SEC (securities) + CFTC (commodities) |

Short version: the GENIUS Act tells Circle and Tether what reserves to hold. The Clarity Act would tell Coinbase, Aave, and Kraken what they can offer you.

The Stablecoin Yield Controversy: The Real Fight

This single provision drives most of the debate around the Clarity Act crypto bill. It’s also the one most likely to hit your wallet and affect you as a crypto holder. Here’s what it says, why banks want it, and why crypto companies are fighting back.

What Section 404 of the Clarity Act Actually Says

Section 404 bans covered digital asset service providers from paying interest or rewards just for holding a stablecoin on their platform. Plain English: no passive yield on centralized platforms.

Here is what is explicitly stated:

No covered party shall, directly or indirectly, pay any form of interest yield solely in connection with holding…payment stablecoins or on a payment stablecoin in a manner that is economically or functionally equivalent to the payment of interest or yield on an interest-bearing bank deposit.

But the real “clarity” falls apart with the exceptions.

The next part of the amendment explicitly permits activity and transaction based rewards and incentives. It sets out a “non-exhaustive list of permissible activity-based or transaction-based rewards or incentives…” Specifically, that list includes:

(i) A transaction, payment, transfer, conversion, remittance or settlement activity, including a rebate or incentive provided in connection with the acceptance or use of a payment stablecoin.

(ii) Providing liquidity for market-making activity, posting of collateral in connection with trading, or otherwise putting assets at credit or investment risk.

(iii) The use of any product or service, including participation in governance, validation, staking or a loyalty, promotional, subscription, or incentive program.

(B) For the avoidance of doubt, payments to restricted recipients of consideration, rewards, or benefits that are permissible pursuant to paragraph (2) and subparagraph (A) may be calculated by reference to balance, duration, tenure, or any combination of the foregoing.

Translation: Crypto platforms can use customer stablecoin deposits to generate returns through activities like lending to other customers or institutions, investing in traditional securities, or locking tokens up for staking.

Real example: you park 1,000 USDC on Coinbase Earn and earn 4.5% APY. That specific setup would be prohibited under Section 404. Yet, Coinbase would be free to do with your deposits what they want. The classic case of “rules for thee, but not for me.”

There’s a possible out. The Tillis/Alsobrooks compromise released in March 2026 could let platforms offer rewards tied to activity, like using the stablecoin for actual transactions or on-platform actions. The exact wording isn’t done yet, and the Senate hasn’t voted on the bill or the compromise.

Why Banks Are Pushing for the Yield Ban

Banks say stablecoin yield is a high-interest savings account in disguise. It competes with them, but without FDIC insurance or capital requirements. It doesn’t take a genius to figure out that banks are worried about a flight of capital from their institutions. Why would you keep your US dollars in a traditional bank savings account for 0.02% interest per year when Coinbase is offering 4.5%?

In their May 2026 statement, the Bank Policy Institute and American Bankers Association warned that yield-earning stablecoins could reduce consumer loans, small-business loans, and farm loans by a fifth or more.

Translation: if you move $10,000 from Chase to USDC on Coinbase for 4.5%, there’s less money in the banking system and fewer mortgages and small-business loans get funded…Not to mention the bank makes less profit.

The bank argument in one sentence: stablecoin yield is a deposit product in disguise, so either regulate it like one or ban it on non-bank platforms.

Why the Crypto Industry Disagrees

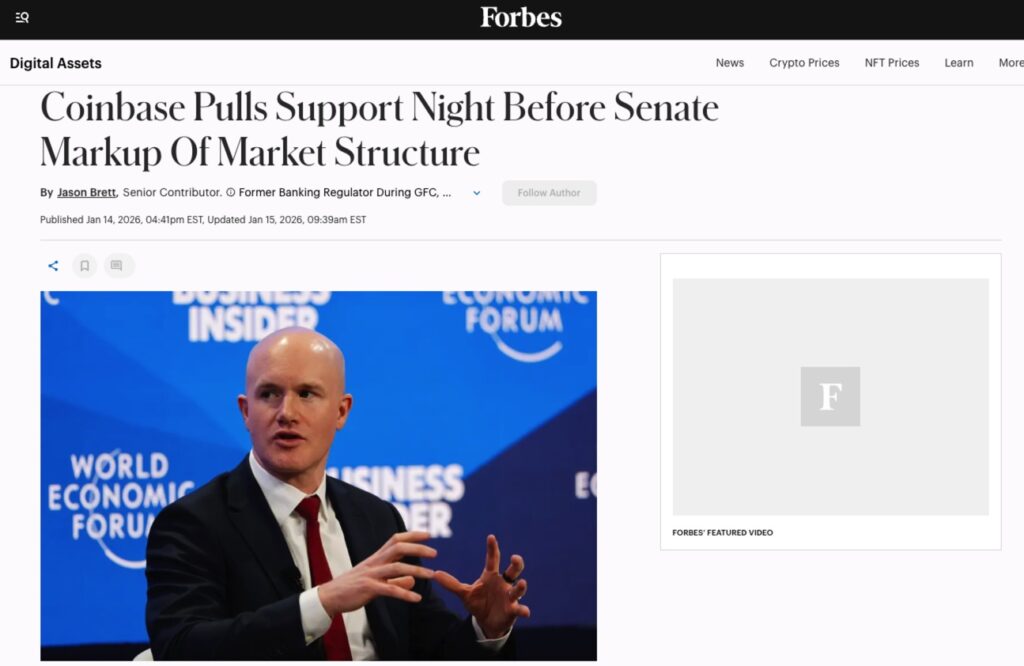

Coinbase withdrew its support for the bill on January 14-15, 2026, calling the yield ban “materially worse than the status quo.” That’s a notable reversal as Coinbase had been one of the bill’s biggest backers.

Money is the reason. Stablecoin yield made up about 20% of Coinbase’s Q3 2025 revenue. This isn’t a side feature. It’s core business.

Crypto companies also make a definitional argument. Stablecoin yield isn’t a deposit, they say. It’s revenue sharing from the T-bill reserves that back the stablecoin, more like a money market fund than a savings account. The yield comes from short-term U.S. Treasury bills the issuer already holds, not from lending your money.

Proponents For and Against the Clarity Act: Where They Stand

The Senate Banking Committee markup of the CLARITY Act is the biggest fight over crypto policy we’ve seen in years. What started as a dry, technical debate about stablecoin reserves has spiraled into a full-blown turf war.

On one side, you have a crypto industry backed into a corner; on the other, an unlikely partnership between traditional banks and organized labor. It’s a strange-bedfellows situation that has completely scrambled the usual alliances in D.C., and it effectively turns a bill about digital assets into a referendum on who gets to control the future of American money.

Proponents: The Institutionalization Camp

The proponents of the Clarity Act view the legislation as a survival mechanism for U.S. competitiveness. Their goal is simple: trade strict oversight for the “regulatory certainty” needed to stop the flight of capital to offshore jurisdictions.

1. Crypto Industry Leaders: The Strategic Pivot

The industry’s stance has shifted from defiance to pragmatism. Coinbase CEO Brian Armstrong, who initially fought the bill’s yield-limiting language, reversed course in April 2026. This pivot likely stems from a desire to finally settle the jurisdictional war between the SEC and CFTC. For industry giants like Galaxy Digital, the act serves as a “durable legislative foundation” that definitively answers the “is it a security?” question, providing a green light for massive institutional inflows.

2. Political Leadership: Dollar Dominance

GOP leaders, led by Senator Thom Tillis (R-N.C.), frame the bill as a way of fostering innovation in the United States. By providing a framework for regulated stablecoins, they aim to ensure the U.S. dollar remains the world’s primary digital medium of exchange. This sentiment is echoed by approximately 78 “Pro-Crypto” Democrats who argue that the status quo: a vacuum of federal oversight, is a greater risk to the economy than the bill’s inevitable compromises.

3. The Treasury Department: Treasury Demand

Secretary Scott Bessent has been the bill’s most vocal advocate within the administration. The Treasury views the Clarity Act’s 1:1 reserve mandate (requiring stablecoins to be backed by Treasuries) as a way to create a permanent, multibillion-dollar “buy” pressure for U.S. debt. In their view, stablecoins are no longer a fringe asset; they are a tool for national fiscal stability.

One more data point: JPMorgan analysts view the overall Clarity Act positively, even with the yield debate unresolved.

Opponents: The Protectionist Camp

Opposition has coalesced around a powerful, if unlikely, coalition that views the bill as a threat to the traditional foundations of the American middle class.

1. The Big Five Labor Unions: The Pension Guard

In a move that caught many by surprise on May 12, 2026, the AFL-CIO, SEIU, AFT, NEA, and AFSCME issued a joint letter to the Senate. Their argument centers on the risk of “embedding” crypto into the real economy without sufficient safeguards. They specifically highlight the threat to public pensions and individual savings, arguing that the Clarity Act socializes the risk of crypto-volatility while privatizing the gains for tech billionaires.

2. The Banking Lobby: The Battle for Deposits

The American Bankers Association (ABA) is fighting an actuarial war. Their primary concern is deposit flight. The ABA estimates that if stablecoins are allowed to offer “rewards” or high DeFi utility under this act, it could lead to a $500 billion exodus from traditional bank accounts by 2028. They are lobbying for a total ban on anything resembling “yield-equivalent” incentives to protect their core business model.

3. Skeptical Democrats: The Ethics Watchdogs

Some lawmakers continue to hammer the bill for being too “industry-friendly.” This group views the 309-page document as a giveaway to the crypto elite, arguing it lacks the necessary ethical guardrails and conflict-of-interest provisions to prevent a repeat of past market collapses. Senator Elizabeth Warren is one such skeptic who argues that some of the bills currently being voted on simply “turbocharge Donald Trump’s crypto corruption.”

Centralized Platforms: How Coinbase Earn and Kraken Are Affected

If you use Coinbase Earn, Kraken’s yield products, or any centralized exchange paying APY on stablecoins, this section is the most relevant to you.

Under current bill language, earning 4.5% APY on USDC just for holding it on Coinbase would be blocked. The platform would need to restructure or drop that product entirely.

What platforms would likely do instead:

- Reframe rewards as “activity-based,” requiring actual transactions to qualify.

- Lower yield rates on restructured products.

- Migrate to brokerage-like structures that look less like deposit accounts.

Coinbase’s decision to pull support over this tells you how big a deal stablecoin yield is for exchanges.

Important: Your USDC principal isn’t at risk. Only the yield feature is. Stablecoins are backed 1:1 by reserves and aren’t banned. Even if Coinbase Earn changes, your principal stays intact.

DeFi Holdings: What Aave, Compound, and Non-Custodial Protocols Face

DeFi protocols work differently from Coinbase Earn, and that difference could carry real weight under the clarity act crypto rules.

On Aave, your funds sit in a smart contract. No company holds your keys or controls your assets. On Coinbase Earn, Coinbase holds your funds in custody. That custodial vs. non-custodial distinction is exactly what the bill’s DeFi exemption hinges on. If a protocol doesn’t “control customer funds,” it may sit outside Section 404’s scope.

The catch: DeFi provisions in the bill are still being written. The Senate version isn’t finalized, and SEC or CFTC rulemaking could narrow or kill the exemption later, even if the original bill text leaves DeFi alone.

Need a refresher on how these protocols work? See what is DeFi.

Clarity Act Risk Level by Platform Type

| Platform Type | Example | Current Risk Level | Why |

| Centralized (custodial) | Coinbase Earn, Kraken | High | Directly targeted by Section 404 yield ban |

| DeFi (non-custodial) | Aave, Compound | Medium | Possible exemption for non-custodial protocols; Senate draft not finalized |

Where Does the Clarity Act Stand Right Now? (May 2026 Update)

The clarity act crypto legislation is alive but stalled in the Senate. Here’s the crypto clarity act news as of mid-2026.

- May 29, 2025: House Financial Services Committee introduces H.R. 3633.

- July 17, 2025: House passes the bill 294-134, with strong bipartisan support.

- July 18, 2025: The GENIUS Act is signed into law the same week, for context.

- January 14, 2026: Senate Banking Committee postpones markup. Over 100 amendments are filed. Coinbase withdraws support over the yield ban.

- March 2026: Tillis/Alsobrooks compromise language on yield released.

- May 2026: Senate Banking Committee hearing held; Senate markup still not scheduled.

- Bonus provision: The bill also bans the Federal Reserve from issuing a central bank digital currency (CBDC) directly to individuals.

Current status: As of May 2026, the Senate Banking Committee hasn’t scheduled a final markup. Prediction markets (Polymarket) put 2026 passage odds at about 72%. The bill is moving, but not fast.

What Should You Do Right Now? A Clarity Act Action Checklist

The clarity act crypto bill isn’t law yet. Nothing about your current holdings is illegal. A little preparation now beats scrambling later.

- Don’t panic: nothing has changed yet. The bill is not law. Your yield positions are legal today.

- Know what you hold and where. Log into Coinbase, Kraken, Aave, and any other platform you use. Note which products pay yield on stablecoins. This is your exposure map.

- Your principal is separate from your yield. USDC is backed 1:1 by reserves and is not at risk. Only the rewards feature is under debate. Want to compare the two main dollar stablecoins? See USDC vs. USDT.

- Watch for platform announcements. Coinbase, Circle, and major DeFi protocols will notify users if products change. Subscribe to their official blogs or newsletters.

- Consider diversifying where you earn. If centralized platform yield concerns you, non-custodial DeFi protocols like Aave and Compound may carry lower regulatory risk under the current bill language.

Regulation is catching up with the market. For long-term holders, a clearer rulebook is ultimately good news.

The Bottom Line

The clarity act crypto bill is the most consequential digital asset market structure legislation in U.S. history. Section 404 is the provision that directly affects retail holders. Whether it passes as written, gets amended, or stalls further will shape how you earn on stablecoins for years.

Nothing has changed yet, and regulatory clarity is ultimately good for the crypto industry and long-term holders.

FAQ: Clarity Act Crypto Questions Answered

Is the Clarity Act already law?

No. The clarity act crypto bill passed the U.S. House 294-134 on July 17, 2025, but the Senate hasn’t voted. The Senate Banking Committee postponed markup in January 2026. As of May 2026, no Senate vote is scheduled. Polymarket prediction markets price 2026 passage at roughly 72%.

Will the Clarity Act ban stablecoin yield on Coinbase?

Section 404 would ban rewards for simply holding a stablecoin on a centralized platform like Coinbase Earn. The bill isn’t law yet. The Tillis/Alsobrooks compromise may allow activity-based rewards (tied to transactions or platform use) to survive. Final language hasn’t been determined.

Does the Clarity Act affect DeFi platforms like Aave?

Possibly, but less certainly than centralized platforms. Non-custodial protocols like Aave and Compound may get an exemption because they don’t hold customer funds — only smart contracts do. The Senate draft isn’t finalized, so the exemption could shrink before passage.

What is the difference between the Clarity Act and the GENIUS Act?

The GENIUS Act, already law as of July 2025, covers stablecoin issuers like Circle and Tether — specifically their reserve requirements. The Clarity Act is a broader market structure bill covering exchanges, DeFi protocols, and platforms that distribute stablecoins. See the comparison table above, or read our full GENIUS Act guide.

Should I move my USDC or USDT out of Coinbase Earn right now?

No urgent need to move yet. The bill isn’t law, and your yield positions are legal today. Map your exposure, watch for official announcements from Coinbase and Circle, and understand the DeFi vs. CeFi risk difference. We’ll update this article as the legislation moves.

References:

“Chairman Scott, Senators Lummis, Tillis Release Market Structure Bill Text Ahead of Banking Committee Markup.” U.S. Senate Committee on Banking, Housing, and Urban Affairs, 8 May 2026, www.banking.senate.gov/newsroom/majority/chairman-scott-senators-lummis-tillis-release-market-structure-bill-text-ahead-of-banking-committee-markup.

“Clarity Act Section 404: Ban on Stablecoin Yield Not Found.” Consumer Federation of America, consumerfed.org/clarity-act-section-404-ban-on-stablecoin-yield-not-found/.

“Coinbase Just Pulled Support for Crypto Legislation Over Yield Restrictions.” Yahoo Finance, 7 May 2026, finance.yahoo.com/markets/crypto/articles/coinbase-just-pulled-support-crypto-075306381.html.

H.R. 3633 – CLARITY Act of 2025. House Committee on Rules, 2025, rules.house.gov/bill/119/hr-3633.

“JPMorgan Says Clarity Act Nearing Finish Line Despite Labor Pushback.” Yahoo Finance, 10 May 2026, finance.yahoo.com/markets/crypto/articles/jpmorgan-says-clarity-act-nearing-165652426.html.

“Regulation by Enforcement.” Financial Services Institute, financialservices.org/advocacy/regulation-by-enforcement/.

S. 1582 – CLARITY Act. Congress.gov, 2026, www.congress.gov/bill/119th-congress/senate-bill/1582.

Sigalos, MacKenzie. “Labor Unions Pressure Congress to Block Crypto Legislation Over Pension Risks.” CNBC, 12 May 2026, www.cnbc.com/2026/05/12/congress-crypto-legislation-labor-unions.html.

“Warren Statement on Lack of Ethics Provisions in Crypto Bill.” U.S. Senate Committee on Banking, Housing, and Urban Affairs, 11 May 2026, www.banking.senate.gov/newsroom/minority/warren-statement-on-no-trump-ethics-provision-in-crypto-bill.

Why you can trust 99Bitcoins

Established in 2013, 99Bitcoin’s team members have been crypto experts since Bitcoin’s Early days.

Weekly Research

100k+Monthly readers

Expert contributors

2000+Crypto Projects Reviewed