In This Article

Every few years, headlines resurface claiming that “Bitcoin mining is finished.” But in 2026, miners are still running warehouses full of machines, the Bitcoin network is stronger than ever, and the industry continues to adapt.

At its core, Bitcoin mining isn’t just about earning coins, it’s the heartbeat of the entire system. Mining secures the blockchain, verifies transactions, and keeps Bitcoin decentralized. Behind the scenes, miners use powerful computers called ASICs to race against each other in solving cryptographic puzzles. The winner gets to add the next block of transactions to the chain and collect rewards in Bitcoin and fees.

Far from being “dead,” mining is evolving. Rising transaction fees, energy innovations, and new players entering the market are reshaping how miners stay profitable. In this guide, we’ll explain what Bitcoin mining is, why it matters, and how the future of mining could look very different from its past.

What is Bitcoin Mining: Summary

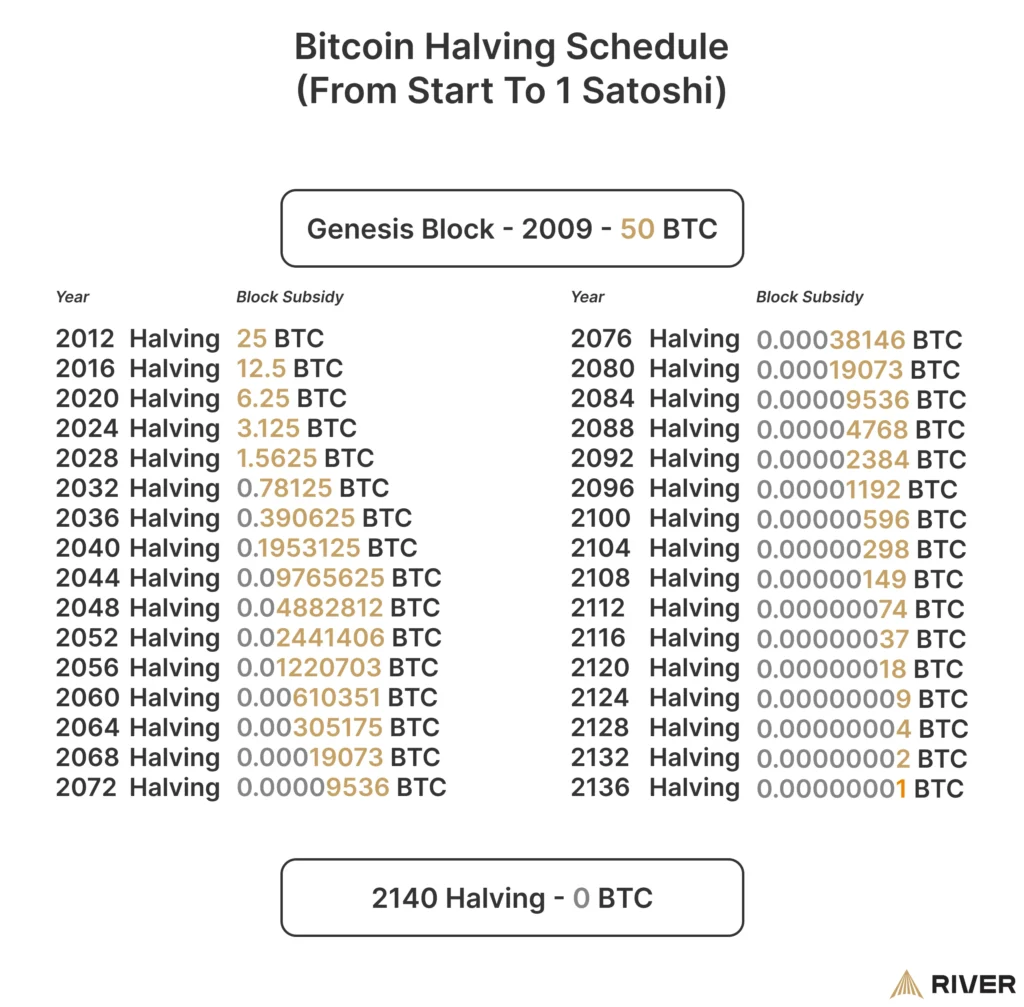

Bitcoin mining is the process of updating the ledger of Bitcoin transactions known as the blockchain. Mining is done by running extremely powerful computers called ASICs that race against other miners in an attempt to guess a specific number. The first miner to guess the number gets to update the ledger of transactions and also receives a reward of newly minted Bitcoins. The Bitcoin block reward was halved in April 2024 to 3.125 BTC. The next halving in 2028 will reduce the reward further to 1.5625 BTC.

Today, to be profitable, you need to invest heavily in Bitcoin mining hardware, cooling, and storage. In 2026, there are other ways to mine Bitcoin without owning hardware, but we will get to it in a bit. For now, just know that it’s not possible to mine Bitcoin profitably with a PC or a GPU at home. You can calculate your profitability using a Bitcoin mining calculator.

Here’s what you’ll need to do to get started with Bitcoin mining:

- Calculate Bitcoin mining profitability 2026

- Get a Bitcoin miner

- Get a Bitcoin wallet

- Find a mining pool

- Download a mining program

- Start mining

Key Takeaways

- Bitcoin mining secures the network by validating transactions and preventing double-spending.

- Miners use ASIC hardware to solve cryptographic puzzles, earning Bitcoin rewards and transaction fees.

- The Bitcoin block reward was halved to 3.125 BTC in 2024 and will drop further to 1.5625 BTC in 2028.

- Mining profitability depends on electricity costs, hardware efficiency, and Bitcoin’s market price.

- Bitcoin mining now also uses renewable energy, making it more sustainable than before.

Don’t like to read? Watch our video guide instead:

What is Bitcoin Mining?

Bitcoin is a decentralized alternative to the banking system, but people have several questions about BTC. This means that the system can operate and transfer funds from one account to the other without any central authority.

With a trusted central authority, transferring money is easy. Just tell the bank you want to remove $50 from your account and add it to someone else’s account. In this example, the bank has all the power because the bank is the only one that is allowed to update the ledger that holds the balances of everyone in the system.

Bitcoin, on the other hand, creates a system that has a decentralized ledger. It gives independent miners the ability to update the ledger without giving them too much power. What does Bitcoin mining mean? It is the process of using specialized computers to validate transactions, secure the Bitcoin network, and receive rewards in Bitcoin for performing this work.

How Cryptocurrency Mining Works

Anyone who wants to participate in updating the ledger of Bitcoin transactions, known as the blockchain, can do so. But how does crypto mining work? All you need is to guess a random number that solves an equation generated by the system.

Sounds simple, right?

Of course, this guessing is all done by your computer. The more powerful your computer is, the more guesses you can make in a second, increasing your chances of winning this game. If you manage to guess right, you earn bitcoins and get to write the “next page” of Bitcoin transactions on the blockchain.

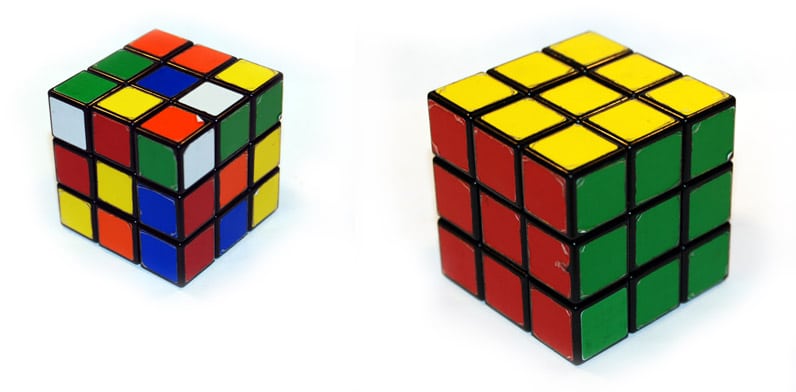

The solution to the equation is very hard to achieve but very easy to validate. You can think of a Rubik’s cube as a good example for this (very hard to solve, but easy to see you’ve solved it).

Rubik’s cube – hard to solve, easy to prove you’ve solved it

The Bitcoin Mining Process in a Nutshell

Once your mining computer comes up with the right guess, your computer determines which pending transactions will be inserted in the next block of transactions on the blockchain. Compiling this block represents your moment of glory, as you’ve now become a temporary banker of Bitcoin who gets to update the Bitcoin transaction ledger. The block of transactions you’ve created, along with your solution, is sent to the whole network so other computers can validate it.

Each computer that validates your solution updates its copy of the Bitcoin transaction ledger with the transactions that you chose to include in the block. The system generates a fixed amount of Bitcoins (currently 6.25 ) and rewards them to you as compensation for the time and energy you spent solving the math problem.

Additionally, you get paid Bitcoin transaction fees that were attached to the transactions you inserted into the next block. All the transactions in the block you’ve just entered are now confirmed by the Bitcoin network and are virtually irreversible.

Bitcoin mining is like a giant lottery where computers race to solve a complex math puzzle every 10 minutes. The first to solve it gets to add a new block of transactions to the Bitcoin network and earns a reward, currently 3.125 BTC plus transaction fees. These puzzles are designed to be incredibly hard to solve but easy to verify, ensuring security and preventing fraud like double-spending (using the same Bitcoin twice). In the early days, anyone could mine Bitcoin with a regular computer, but now the difficulty is so high that miners use specialized machines (ASICs) that are expensive and power-hungry.

Here’s a two-minute video showing the process of blocks and confirmations.

It’s called mining because of the fact that this process helps “mine” new Bitcoins from the system. But if you think about it, the mining part is just a by-product of the transaction confirmation process. So the name is a bit misleading, since the main goal of mining is to maintain the ledger in a decentralized manner.

Since mining is based on a form of guessing, each time a different miner will guess the number and be granted the right to update the blockchain. Of course, the miners with more computing power will succeed more often, but due to the law of statistical probability, it’s highly unlikely that the same miner will succeed every time.

Effects on the Environment and Energy Efficiency

It is impossible to overlook the environmental impact of mining. Bitcoin mining uses a lot of electricity—roughly 121 TWh in 2023, or 0.44% of world consumption—and produces plenty of e-waste because of outdated hardware. Miners can reduce their impact and prepare for the future by emphasizing the use of renewable energy and efficiency improvements.

Bitcoin Mining Difficulty

Now that you know what Bitcoin mining is, you might be thinking, “Cool! Free money! Where do I sign up?” Well, not so fast.

Satoshi Nakamoto, Bitcoin’s inventor, crafted the rules for mining in a way that the more mining power the network has, the harder it is to guess the answer to the mining math problem. So the difficulty of the mining process is self-adjusting to the accumulated mining power the network possesses.

If more miners join, it will get harder to solve the problem; if many of them drop off, it will get easier. This is known as mining difficulty.

Mining difficulty adjusts every 2,016 blocks

Difficulty Adjustment

Difficulty is self-adjusting to create a steady flow of new Bitcoins into the system. In a sense, this was done to keep inflation in check. Mining difficulty is set so that, on average, a new block will be added every ten minutes (i.e., the number will be guessed every ten minutes on average).

Now, remember, this is on average. We can have two blocks being added minute after minute, and then wait an hour for the next block. In the long run, this will even out to ten minutes on average.

The difficulty adjustment is done every 2,016 blocks (every 2 weeks on average) retroactively. Meaning, every 2,016 blocks, the system looks back on the past 2016 blocks and calculates the average block time. If it’s under 10 minutes, it will increase the difficulty; if it’s over 10 minutes, it will lower it.

Due to heatwave-related hashrate drops, the network had a significant 7.5% reduction in late June 2025, the biggest since 2021, following months of increasing difficulties. 2025 is seeing a slowdown in difficulty growth, which could be the lowest annual increase ever.

Bitcoin Mining Hardware

Before we jump into this section, it is important to note that ASIC miners have been the standard since 2013, and CPU, GPU, or FPGA mining is no longer relevant for profitable Bitcoin mining.

CPU Mining

When Bitcoin first started, there weren’t a lot of miners out there. Satoshi, the inventor of Bitcoin, and his friend Hal Finney were a couple of the only people mining Bitcoin back at the time with their personal computers.

Using your CPU (central processing unit—your computer’s brain) was enough for mining Bitcoin back in 2009, since the mining difficulty was very low. As Bitcoin started to catch on, people looked for more powerful mining solutions.

GPU Mining

A GPU (graphics processing unit) is a special component added to computers to carry out more complex calculations. GPUs were originally intended to allow gamers to run computer games with intense graphics requirements.

Because of their architecture, GPUs became popular in the field of cryptography, and around 2011, people also started using them to mine Bitcoins. For reference, the mining power of one GPU equals that of around 30 CPUs.

FPGA Mining

FPGA is a piece of hardware that can be connected to a computer in order to run a set of calculations. They are just like GPUs but 3–100 times faster. The downside is that they’re harder to configure, which is why they weren’t as commonly used in mining as GPUs.

ASIC Mining

Around 2013, a new breed of miner was introduced: the ASIC miner. ASIC stands for Application Specific Integrated Circuit. ASICs are pieces of hardware manufactured solely for mining Bitcoin. Unlike GPUs, CPUs, and FPGAs, they couldn’t be used to do anything else. Their function was hardcoded into the machine.

Today, ASIC miners are the current mining standard. Bitcoin mining has become entirely ASIC-dominated, and mining with PCs or GPUs is not just unprofitable—it’s practically obsolete. Some early ASIC miners even appeared in the form of a USB, but they became obsolete rather quickly. Even though they started in 2013, the technology quickly evolved, and new, more powerful miners were coming out every six months.

After about three years of this crazy technological race, we finally reached a technological barrier, and things started to cool down a bit. Since 2016, the pace at which new miners are released has slowed considerably.

Canaan CEO Nangeng Zhang sees Bitcoin mining evolving with efficiency gains, new energy sources, and AI integration. He predicts “over 20% efficiency gains per year” despite slowing ASIC advancements. He highlighted in an interview that the Middle East is a growing mining hub with “welcoming regulations.”

Difference Between ASICs and GPUs

ASIC miners generate significant heat and noise, often requiring industrial-scale cooling solutions, while GPUs are quieter and more versatile, making them easier to repurpose for gaming, AI, or other computing tasks. Companies, like Nvidia, are also investing in virtual GPUs. Here is how the two compare:

| Parameter | ASIC Miners | GPU Miners |

| Initial Cost | High ($3,000 – $10,000 per unit) | Lower ($500 – $2,000 per unit) |

| Hash Rate | Very High (TH/s range) | Lower (MH/s range) |

| Energy Efficiency | High (More hashes per watt) |

Lower (Higher power consumption)

|

| Power Usage | 1,500W – 5,500W | 200W – 1,200W per GPU |

| Mining Algorithms | Limited (Algorithm-specific) | Versatile (Supports multiple coins) |

| Flexibility | Low (Dedicated to one coin type) | High (Can switch between coins) |

| Longevity | Becomes obsolete faster | Lasts longer |

| Resale Value | Lower (Hard to resell after updates) | Higher (Used for gaming/AI) |

| Ease of Setup | More complex (Cooling required) | Easier to set up |

| Best Use Case | Large-scale mining operations | Small-scale or multi-coin mining |

Bitcoin Mining Pools

Mining is an extremely competitive game. Even if you buy the best possible miner out there, you’re still at a huge disadvantage compared to professional Bitcoin mining farms. That’s why mining pools came into existence.

The idea is simple: miners group to form a “pool” so they can combine their mining power and compete more effectively. Once the pool manages to win the competition, the reward is spread out among the pool members depending on how much mining power each of them contributed.

This way, even small miners can join the mining game and have a chance of earning Bitcoin (though they get only a part of the reward).

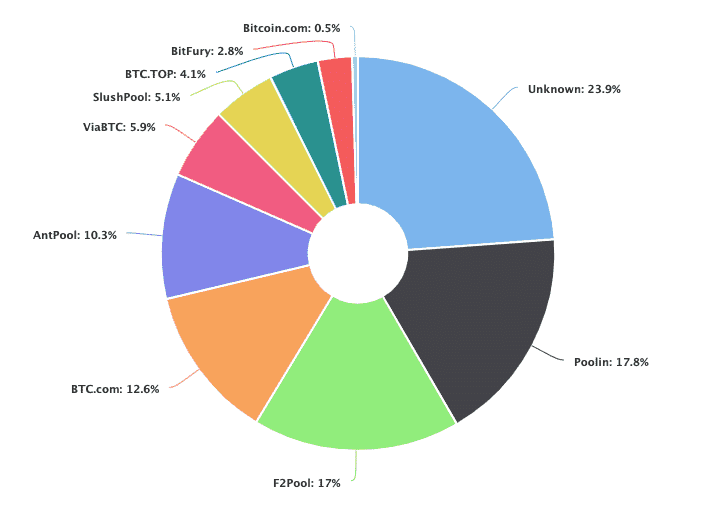

The market share of the most popular Bitcoin mining pools in 2020

Today, there are over a dozen large pools that compete for the chance to mine Bitcoin and update the ledger. Since China banned Bitcoin mining in 2021, mining operations have shifted to North America, Kazakhstan, Russia, and the Middle East. The U.S. now leads in mining hashrate, with Texas being a major hub due to its cheap energy and mining-friendly policies.

Is Bitcoin Mining Profitable?

The short answer for some is “probably not”; Many ask, can you still mine Bitcoin? The correct answer is “it depends on a lot of factors.” A report by Fidelity Digital noted that miners must constantly expand operations to remain competitive.

“Miners cannot afford to just maintain their position in the network. Instead, they must constantly push to acquire more hash rate as well as increase the efficiency of their hash rate, acquire lower-cost energy from cheaper sources, and expand their infrastructure,” the report added.

When calculating Bitcoin mining profitability, there are a lot of things you need to take into account. For instance, using a Bitmain S21 XP+ Hyd (500TH/s, 5500W) at an electricity rate of $0.10/kWh, mining costs would be $13.20 per day in electricity while generating approximately 0.00028 BTC per day. This means profitability is highly dependent on Bitcoin’s market price and electricity costs in your region.

Let’s break them down further.

Hashrate (How Powerful is Your Miner)

A Hash is the mathematical problem the miner’s computer needs to solve. The hashrate refers to your miner’s performance (i.e., how many guesses your computer can make per second).

Hashrate can be measured in MH/s (mega hash = 1m hashes per second), GH/s (giga hash = 1b hashes per second), TH/s (terra hash = 1t hashes per second), and even PH/s (peta hash = 1000t hashes per second).

Bitcoin Reward

The number of Bitcoins generated when a miner finds a solution (in other words, “solves a block”). This number started at 50 bitcoins back in 2009, and it’s halved every 210,000 blocks (about four years). The current number of Bitcoins awarded per block is 3.125.

The last block-halving occurred in April 2024, and the next one will be in 2028. Once the halving occurs, the reward will decrease to 1.5625 Bitcoin.

Mining Difficulty

A number that represents how hard it is to mine bitcoins at any given moment, considering the amount of mining power currently active in the system.

Electricity cost

Also known as “how many dollars are you paying per kilowatt to get electricity?”

You’ll need to find out your electricity rate in order to calculate profitability. This can usually be found on your monthly electricity bill. The reason this is important is that miners consume electricity, whether for powering up the miner or for cooling it down (these machines can get hot and noisy).

Power consumption

Each miner consumes a different amount of energy. You’ll need to find out the exact power consumption of your miner before calculating profitability. This can be found easily with a quick search online. Power consumption is measured in watts.

Pool fees

If you’re mining through a mining pool, then the pool will take a certain percentage of your earnings for rendering their service. Generally, this would be somewhere around 2%.

Bitcoin’s price

Since no one knows what Bitcoin’s price will be in the future, it’s hard to predict whether Bitcoin mining will be profitable. If you are planning to convert your mined bitcoins to any other currency in the future, this variable will have a significant impact on profitability.

Legal Clarity & Tax Implications

Legal and tax frameworks for Bitcoin mining vary significantly by country.

Difficulty Increases per Year

This is probably the most important and elusive variable of them all. The idea is that since no one can predict the rate of miners joining the network, neither can anyone predict how difficult it will be to mine in six weeks, six months, or six years from now.

In all the time Bitcoin has existed, its profitability has dropped only a handful of times, even at times when the price was relatively low.

The last two factors (price and difficulty increase) are the reasons no one will ever be able to give a 100% accurate answer to the question “is Bitcoin mining profitable?”

Once you have all of these variables at hand, you can insert them into a Bitcoin mining calculator (as can be seen below) and get an estimate of how many Bitcoins you will earn each month. If you can’t get a positive result on the calculator, it probably means you don’t have the right conditions for mining to be profitable.

[ccpw id=”167160″]Solo Mining: A Bitcoin Lottery Ticket

Solo mining is when an individual miner runs their own equipment without joining a mining pool. Instead of combining computing power with others, you’re on your own. If your machine finds the winning hash, you get the full block reward and all the transaction fees.

But here’s the catch: the odds are extremely slim. With Bitcoin’s network difficulty at record highs, a small solo mining setup is unlikely to win a block in any reasonable amount of time. For most people, solo mining today is more like buying a lottery ticket, you could hit a big payout, but the chances are vanishingly small.

That said, some enthusiasts still do it for fun, or for the slim possibility of striking gold without having to share the reward. In practice, though, mining pools remain the only viable option for consistent earnings.

Step-by-Step Guide for Mining at Home

If you want to know how to get started in cryptocurrency mining, follow these steps to set up your first secure Bitcoin miner:

Step 1: Calculate Profitability

Before even starting with Bitcoin mining, you need to do some research. The best way to do this, as we’ve discussed, is through the use of a Bitcoin mining profitability calculator.

Bear in mind that mining needs money. If you don’t have a few thousand dollars to spare on the right miner, and if you don’t have access to cheap electricity, mining Bitcoin might not be for you.

Step 2: Get a Miner

Once you’re done with your calculations, it’s time to get your miner! Make sure to go over our Bitcoin mining hardware reviews to understand which miner is best for you, if you haven’t done it already in step 1. Here’s a list of the most popular miners around today:

You can purchase mining hardware directly from the manufacturers or buy it on second-hand markets such as eBay or Amazon.

Step 3: Get a Bitcoin Wallet

You’ll need a Bitcoin wallet for your newly mined Bitcoin. Once you have a wallet, make sure to get your wallet address; it will be a long sequence of letters and numbers.

Each wallet has a different way of getting to the Bitcoin address, but most wallets are pretty straightforward about it. Notice that you’ll need your Bitcoin address and NOT your private key (which is like the secret password for your wallet).

Step 4: Find a Mining Pool

When you join a mining pool, you’ll be given only part of the math problem to solve. The combined work of all of the miners in the pool will make the pool more likely to solve the original problem and earn the bitcoin reward and transaction fees. The profits will be spread out throughout the pool based on contribution.

Basically, you’ll make a more consistent amount of Bitcoins and will be more likely to receive a return on your investment.

When choosing which mining pool to join, make sure to ask the following questions:

- What is the reward method? (Proportional/Pay Per Share/Score Based/PPLNS—more on that here)

- What fee does the pool charge for mining and the withdrawal of funds?

- How frequently does the pool find a block (i.e., how frequently do I get rewarded)?

- How easy is it to withdraw funds?

- What kind of stats does the pool provide?

- How stable is the pool?

To answer most of these questions, you can use our Bitcoin mining pools review or this excellent post from BitcoinTalk. You can also find a complete comparison of mining pools in the Bitcoin wiki.

Once you are signed up with a pool, you’ll get a username and password for that specific pool, which you will use later on.

Step 5: Get a Mining Program (Also Known as a Client)

Controlling and monitoring your mining hardware requires dedicated software. Depending on what mining rig you have, you’ll need to find the right software.

Many mining pools have their own software, but some don’t. In case you’re not sure which mining software you need, you can find a list of Bitcoin mining software here. Also, if you want to compare different mining software, you can do it here.

Step 6: Start Mining!

Connect your miner to a power outlet and fire it up. Make sure to connect it to your computer as well (usually via USB) and open up your mining software. The first thing you’ll need to do is to enter your mining pool’s address, username, and password.

Once this is configured, you will start collecting shares, which represent your part of the work in finding the next block. According to the pool you’ve chosen, you’ll be paid for your share of coins—just make sure that you enter your address in the required fields when signing up for the pool.

Pro tip: If you’re looking for an easy way to earn small amounts of Bitcoin without mining, using a Bitcoin Faucet can be a great option. These websites reward users with Bitcoin for completing simple tasks. One of our personal favorites is the Lolli app, which offers a daily faucet as well as Bitcoin back shopping rewards.

Additional Types of Mining

Cloud Mining

Cloud mining allows users to participate in crypto mining without owning physical hardware. Cloud mining means that you do not buy a physical mining rig but rather rent computing power from a mining company and get paid according to how much mining power you own.

At first, this sounds like a really good idea, since you don’t have to go through all of the hassle of buying expensive equipment, storing it, cooling it, and monitoring it.

However, when you do the math, it seems that most of these cloud mining sites aren’t profitable. Those that do seem profitable are usually scams that don’t even own any mining equipment; they’re just elaborate Ponzi schemes that will end up running away with your money.

If you still want to pursue this path, make sure to make the right calculations before handing over any funds. Also, review the terms and conditions closely.

Some cloud mining services have no guarantee when you look at the platform a little closer. If you decide to try cloud mining, look for a cloud mining company with a guaranteed return on your investment, like Coin Mining Farm. This platform has a liquidity pool to help protect your investment if the price of Bitcoin drops severely.

Mining on a Mobile Phone

Some mobile apps claim to mine Bitcoin on your phone. While in theory, this is possible, due to the low processing power phones have compared to ASIC miners, you’ll probably end up draining your phone’s battery much faster and make a very small fraction of Bitcoin in return.

The apps that allow this act as mining pools for mobile phones and distribute earnings according to how much work was done by each phone.

Remember, mining is possible with any old computer—it’s just not worth the electricity wasted on it because the slower the computer, the smaller the chances are of actually getting some kind of reward.

For reference, mining was demonstrated in theory on a 55-year-old computer some time ago by IBM, and the result was, of course, that it’s not worth it.

Web Mining

Somewhere around 2017, the concept of web mining or ‘cryptojacking’ was introduced. Simply put, web mining allows website owners to “hijack” visitors’ CPU power and use it to mine Bitcoin.

This means that a website owner can make use of thousands of “innocent” CPUs in order to gain profits. However, since mining Bitcoins isn’t really profitable with a CPU, most of the sites that utilize web mining mine Monero instead. Up until today, over 20,000 sites have been known to utilize web mining.

The concept of web mining is very controversial. From the site’s visitor perspective, someone is using their computer without consent to mine Bitcoins. In extreme cases, this can even harm the CPU due to overheating.

From the site owner’s perspective, web mining has become a new way to monetize websites without the need for the placement of annoying ads. Also, the site owner can control how much of the visitor’s CPU he wants to use in order to make sure he’s not abusing his hardware.

For more information about web mining, you can read this post.

To estimate mining profitability, you can use a Bitcoin Mining Calculator. This tool helps miners calculate expected earnings based on several factors.

|

Mining Method |

Hardware Needed |

Cost |

Profitability |

Flexibility |

Energy Use |

Best For |

|

ASIC Mining |

Specialized ASIC miners |

High ($3,000 – $10,000 per unit) |

High (If electricity is cheap) |

Low (Only for BTC) |

Very High (1,500W – 5,500W) |

Large-scale mining farms |

|

GPU Mining |

High-end GPUs (Nvidia, AMD) |

Medium ($500 – $2,000 per GPU) |

Low (Not profitable for BTC) |

High (Can mine other coins) |

Moderate (200W – 1,200W) |

Altcoin miners, hobbyists |

|

Cloud Mining |

None (Rent hash power) |

Varies (Subscription-based) |

Low (Often not profitable) |

Low (Locked into contract) |

Depends on provider |

Those who don’t want to buy hardware |

|

Mobile Mining |

Smartphone apps |

Low (Free or small fees) |

Very Low (Tiny rewards) |

High (Mine anywhere) |

Low (But drains battery) |

Beginners, fun experiments |

|

Web Mining |

Browser-based scripts |

None (Uses CPU power) |

Very Low (Slow and inefficient) |

Medium (No setup needed) |

Low (Uses user’s CPU) |

Websites monetizing user visits |

|

FPGA Mining |

FPGA chips |

Medium-High ($1,000 – $5,000) |

Medium (More efficient than GPU) |

Medium (Reconfigurable) |

Medium (More efficient than GPUs) |

Experienced miners experimenting with efficiency |

|

Hybrid AI + Mining |

AI data center integration |

Very High |

Emerging (Future trend) |

Medium (Used for AI + BTC) |

High (Data center energy use) |

Large companies, AI-powered mining |

Conclusion: Is Bitcoin Mining Worth It?

Bitcoin mining profitability continues to hinge on one of the most important variables: electricity costs. By 2026, Bitcoin has reached price levels that few predicted a decade ago, but the economics of mining remain challenging. Following the 2024 halving, block rewards dropped to 3.125 BTC, meaning miners now earn less for the same amount of work. For industrial-scale operations with access to cheap electricity, often sourced through hydro, solar, or even excess flared gas, mining can still generate healthy margins. However, for small-scale miners or hobbyists, the path is far less certain. Equipment costs, ongoing energy bills, and network difficulty adjustments can quickly outweigh potential returns if not carefully considered in advance.

Another ongoing point of debate is Bitcoin’s environmental footprint. While critics point to its high energy usage, the industry has been steadily adopting more sustainable practices. Increasingly, miners are setting up operations in areas rich in renewable resources, using stranded energy, or repurposing wasted energy streams that would otherwise go unused.

That said, mining is not always the most effective way to gain exposure to Bitcoin. In many cases, simply buying BTC outright may provide a better return without the operational risks of running hardware. Investors can also explore mining altcoins such as Monero or Zcash, which remain accessible through GPUs, or experiment with lightweight options like browser-based mining platforms. Ultimately, whether you choose to mine or invest directly, the key is understanding your costs, risk tolerance, and long-term strategy in the evolving world of digital assets.

See also:

- What is a Bitcoin IRA? A Beginners Guide

- How Many Bitcoins Are There in 2026 & How Many Are Left?

- Is Bitcoin Money?

- What is the Lightning Network? A Simple Explanation

FAQs

How Much Does it Cost to Mine 1 Bitcoin in 2026?

The cost to mine 1 Bitcoin depends on electricity rates, hardware efficiency, mining difficulty, and operational expenses like cooling and maintenance.

How Many Bitcoins Can You Mine in a Day?

The number of Bitcoins you can mine in a day depends on your mining hardware’s hashrate and the network difficulty. Using the Bitmain Antminer S21 XP+ Hyd (500TH/s, 5500W) as an example, this miner produces ~0.00028 BTC per day.

What Will Happen When All Bitcoins Are Mined?

What will happen when all of 21 million Bitcoins are mined? When all 21 million Bitcoins are mined (estimated to happen in 2140), miners will no longer receive block rewards. Instead, they will earn income from transaction fees, which users pay to have their transactions processed. Currently, miners receive both newly minted Bitcoins and transaction fees, but over time, as block rewards decrease, fees will play a bigger role. If Bitcoin remains valuable and widely used, these fees should continue to incentivize miners to secure the network. The shift to a fee-based model ensures that mining remains viable even after the last Bitcoin is mined.

Is it Illegal to Mine Bitcoin in 2026?

Bitcoin mining is legal in most countries, but regulations vary by region. Some nations, like China, have banned mining due to energy concerns, while others, like the U.S. and Canada, allow it with certain regulations. In countries with no clear stance, such as many African nations, mining remains unregulated but not illegal. It’s important to keep a close eye on the friendliness of countries towards mining, because the regulatory environment could change at the drop of a hat.

Isn’t Bitcoin Mining a Waste of Electricity in 2026?

Bitcoin mining has been criticized for its high energy consumption, but it is also driving innovation in renewable energy and energy optimization. A UN climate body has suggested implementing a climate tax on each kWh consumed by cryptocurrency miners to reduce emissions. This is an evolving global policy consideration.

Many mining operations now use hydroelectric, solar, or surplus energy that would otherwise go to waste. Additionally, Bitcoin mining helps stabilize power grids by consuming excess energy during low-demand periods. While mining does require electricity, its impact depends on where and how the energy is sourced, with an increasing shift towards sustainable and efficient solutions.

Can’t Google Start Mining Bitcoin and Dominate the Competition in 2026?

While Google has immense computing power, its servers are not optimized for Bitcoin mining. Bitcoin mining requires specialized ASIC (Application-Specific Integrated Circuit) miners, which are far more efficient than general-purpose servers. Even if Google dedicated all its data centers to mining and abandoned its core business, it would contribute less than 0.001% of Bitcoin’s total network hashrate. The Bitcoin mining industry is dominated by ASIC-powered mining farms, making it impractical for companies like Google to compete using traditional hardware.

How to Get Started in Cryptocurrency Mining?

To start cryptocurrency mining, you need specialized mining hardware (ASIC or GPU), mining software, a digital wallet to store earnings, and access to cheap electricity. You’ll also need to join a mining pool to combine resources with other miners for better chances of earning rewards. Before investing, use a mining profitability calculator to check if mining is worth it based on electricity costs and hardware efficiency.

What Is Mining Bitcoin Mean?

Bitcoin mining refers to the process of validating Bitcoin transactions and adding them to the blockchain. Miners use powerful computers to solve complex mathematical problems, and the first to find a valid solution gets rewarded with newly minted Bitcoin. This process secures the network and ensures transactions are legitimate.

How Does Bitcoin Mining Work?

Bitcoin mining works by using specialized hardware to solve cryptographic puzzles that secure the network. Miners compete to guess a number that validates a block of transactions. The first miner to solve it adds the block to the blockchain and earns a block reward plus transaction fees. Mining difficulty adjusts over time to keep block production steady at about every 10 minutes.

How Long Will It Take to Mine 1 Bitcoin?

The time required to mine 1 Bitcoin depends on your mining hardware, electricity costs, and network difficulty. Using a Bitmain Antminer S21 XP+ Hyd (500TH/s, 5500W), it would take about 3,571 days (~9.8 years) to mine 1 BTC alone. However, miners usually join mining pools to combine their power and earn smaller but frequent rewards.

How Do Bitcoin Miners Make Money?

Bitcoin miners make money by earning block rewards (newly minted Bitcoin) and transaction fees from processing transactions. The block reward is halved approximately every four years. Miners also receive fees from users who pay extra to have their transactions processed faster. Profitability depends on electricity costs, mining difficulty, and Bitcoin’s price.

What Is GH/s in Bitcoin Mining?

GH/s (Gigahashes per second) is a unit of measurement that indicates how many cryptographic calculations (hashes) a miner can perform per second. Mining hardware is measured in MH/s (Megahashes), GH/s, TH/s (Terahashes), and PH/s (Petahashes). More hashes per second mean a higher chance of successfully mining a Bitcoin block.

Can Bitcoin Mining Be Traced?

Bitcoin mining itself cannot be directly traced, but the Bitcoin transactions miners process are recorded on the public blockchain. While mining pools and exchanges may track miners’ activities, individual miners using privacy tools, VPNs, or anonymous wallets can reduce their traceability. However, governments can monitor electricity usage and mining-related internet traffic to detect large-scale mining operations.

References

- Lumerin Blog. “ASICs vs. GPU Mining Rigs: Which One Is Best for You?” Medium, https://medium.com/lumerin-blog/asics-vs-gpu-mining-rigs-which-one-is-best-for-you-3e0175c012b2.

- Foreman. “Ultimate Guide to Bitcoin Mining Hardware: ASICs, Infrastructure, Cooling & More.” Foreman Blog, https://foreman.mn/blog/ultimate-guide-to-bitcoin-mining-hardware-asics-infrastructure-cooling-more/.

- u/mineshop. “What’s Better: ASIC or GPU Miners?” Reddit, r/BitcoinMining, https://www.reddit.com/r/BitcoinMining/comments/10lplqy/whats_better_asic_or_gpu_miners/?rdt=48389.

- Bitcoin Developer Guide. “Mining.” Bitcoin.org, https://developer.bitcoin.org/devguide/mining.html.

- American Geophysical Union (AGU). “Bitcoin Mining Has Very Worrying Impacts on Land and Water, Not Only Carbon.” AGU News, https://news.agu.org/press-release/bitcoin-mining-has-very-worrying-impacts-on-land-and-water-not-only-carbon/.

Why you can trust 99Bitcoins

Established in 2013, 99Bitcoin’s team members have been crypto experts since Bitcoin’s Early days.

Weekly Research

100k+Monthly readers

Expert contributors

2000+Crypto Projects Reviewed