There is a problem that gets talked about less than it should be. Crypto holders sitting on significant unrealized gains – sometimes years of them – often have no easy way to access that value. Selling triggers a taxable disposal in most jurisdictions. Holding indefinitely means watching potential liquidity sit locked inside a wallet.

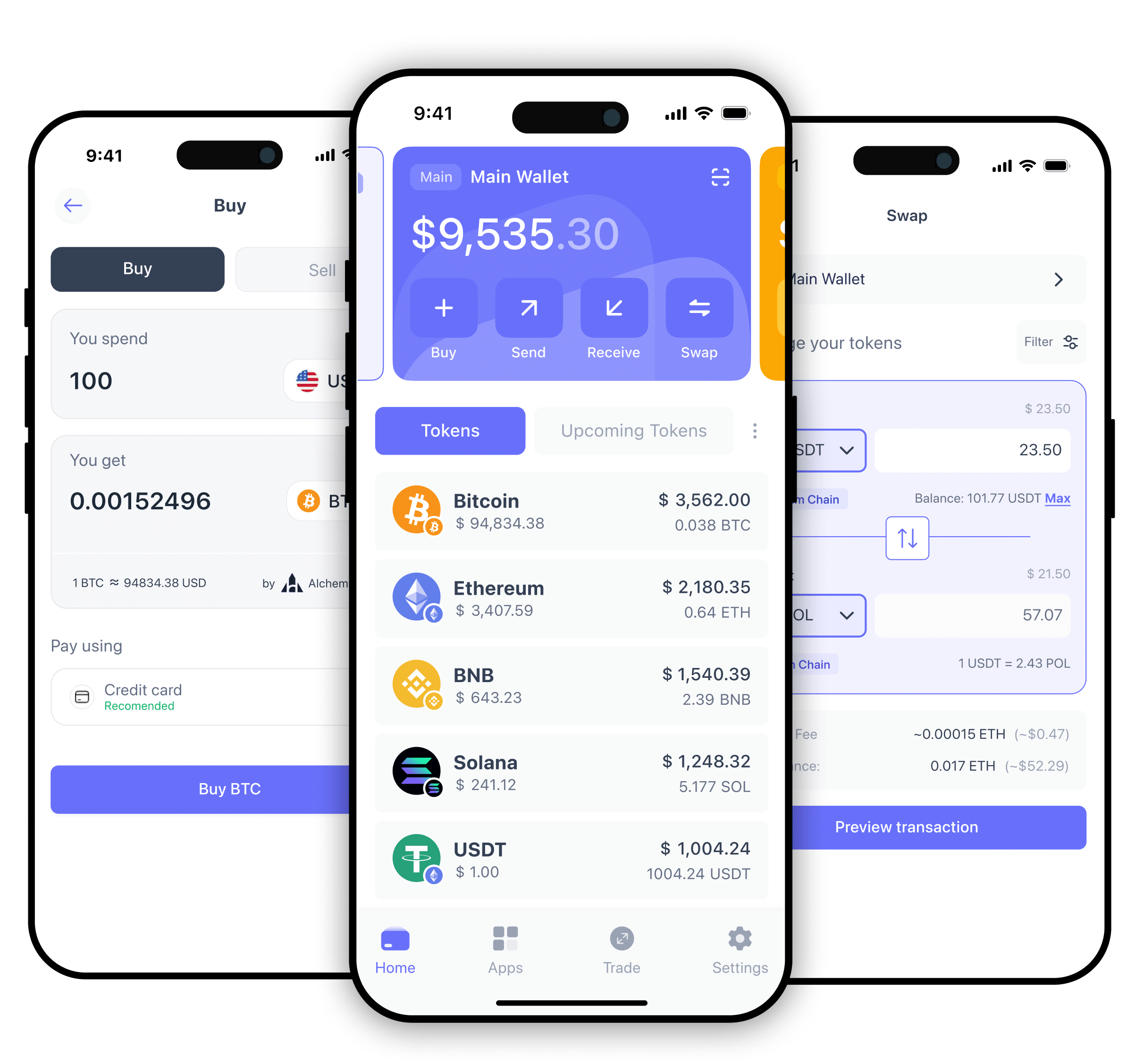

The product itself is not complicated: you deposit crypto as collateral, receive stablecoins (USDT, USDC, or JPYC), retain ownership of your underlying asset, and repay in full when ready.

Clend means you do not have to sell. The platform lets you pledge your crypto holdings as collateral, receive stablecoins in return, and repay the full amount when you are ready – without your underlying position ever changing hands.

In many jurisdictions, that means no disposal event occurs at the point of borrowing, and no capital gains event is recognized. Whether that applies to you depends on where you live and your individual tax situation, so knowing your own situation is important. But the service has obvious appeal for anyone sitting on a substantial unrealized gain they would rather not trigger.

The service runs in English and Japanese, with a dedicated platform for Japanese users. That is not a coincidence, as Japan currently taxes crypto profits at rates of up to a hefty 55%.

Our Clend review explores the rates, the benefits and caveats, ease-of-use, and what type of crypto holder can benefit the most.

Clend offers crypto-backed loans in USDT, USDC, and JPYC against 19 digital assets, with annual rates running from 6.0% on Bitcoin up to 16.80% on smaller-cap altcoins. On BTC, we were unable to find better rates. There are no monthly payments – unpaid interest folds into the outstanding balance each month, and the full amount is settled at the end of the loan. Security is strong, with collateral secured through Fireblocks’ institutional custody infrastructure. Loans are available for up to 12 months, with a minimum borrowing amount of 30,000 USDC and a minimum collateral value of approximately 33,000 USD. It is a fantastic service if the maths works for you, albeit arguably built for high-net-worth individuals and corporate borrowers (say, Web3 treasuries or long-term BTC holders who want stablecoin liquidity without disturbing the underlying position). Our Verdict on Clend

Pros

Cons

What Is Clend?

Clend is based in New York City and is built specifically for crypto borrowing services. There is no trading, no yield product, no governance token, and no yield-boosting tier that rewards loyalty with better rates. Instead, the entire platform does one thing: it loans stablecoins against crypto collateral at a dependable, fixed annual rate, secured through institutional custody infrastructure, with full repayment due at the end of the term.

We see that focus as a feature rather than a limitation, with the service giving transparent terms, consistent rates, and no shenanigans around holding platform assets or meeting eligibility conditions beyond passing KYC and meeting the collateral levels.

Both individual and corporate borrowers can apply, although the minimum collateral value of ~33,000 USD makes the service most relevant to high-net-worth holders and Web3 companies managing crypto-denominated treasuries.

The latter use case is more common than it might seem – crypto-native firms with BTC or ETH on the balance sheet often need operating capital without wanting to liquidate long-term holdings.

The Japanese market focus is worth noting separately, with a dedicated Japanese-language platform. For a Japanese investor sitting on a large BTC gain who needs liquidity this year, the difference in total costs between selling or buying is likely significant.

Clend Key Takeaways

Type

Centralized Crypto Lending (CeFi)

Operator

R0 Inc.

Headquarters

New York City, USA

Markets

English and Japanese

Supported Collateral

19 digital assets

Minimum Loan

30,000 USDC

Minimum Collateral

~33,000 USD equivalent

Disbursement Currencies

USDT, USDC, JPYC

Supported Networks

ERC-20, BSC, TRON, Polygon, Omni (USDT); ERC-20 (USDC)

Annual Rate Range

6.0% – 16.80% (fixed, nominal)

Maximum Term

12 months

Custody

Fireblocks MPC-CMP + HSMs, SOC 2 Type 2

Monthly Payments

None

Liquidation Trigger

Loan balance at 90% of collateral value (95% for stablecoins)

Fees

None beyond the stated interest rate

How the Lending Model Works

Clend describes its approach as overcollateralized lending, meaning the collateral must exceed the loan amount at all times. The maximum loan-to-value (LTV) at origination varies by asset – 60% for BTC and ETH, 40% for most altcoins, and 90% for stablecoin collateral – so there is a built-in buffer from day one.

Unlike platforms that put deposited collateral to work generating yield, Clend holds the assets in custody without deploying them elsewhere. There is no fractional-reserve component and no collateral rehypothecation. Clend’s explanation for its low starting rates is that this custody-only model keeps its cost structure simple – it is charging for the loan, not making money on both sides of the collateral.

Custody runs through Fireblocks, which provides institutional-grade digital asset security for major financial institutions worldwide. The specific technology Clend uses is Fireblocks’ MPC-CMP. The Fireblocks infrastructure carries SOC 2 Type 2 compliance certification and is subject to ongoing third-party audits.

The interest model is unusual compared to most lending products, with no monthly payment obligations. Instead, each month’s unpaid interest is automatically added to the outstanding balance, increasing the loan amount over time. The borrower settles the entire amount – original principal plus all accumulated interest – when they repay. Full repayment is available starting on day 61 after the contract is signed, and partial repayments can be made at any time.

The rates Clend publishes are nominal annual figures, calculated by multiplying the monthly rate by 12. Because interest compounds monthly rather than accrues on a simple basis, the effective annual rate will be slightly above the stated figure.

Understanding Liquidation

How Clend handles liquidation is one of the platform’s more unique aspects, and it is worth understanding precisely.

On most lending platforms, liquidation is triggered when the collateral’s value falls below a set price threshold relative to the loan amount. Clend’s trigger works differently, in that liquidation occurs when the outstanding loan balance – which grows each month as interest compounds – reaches 90% of the collateral’s value at that moment. For loans backed by stablecoin collateral, the threshold is 95%.

The practical implication is that a sudden short-term price drop does not automatically put a borrower’s collateral at risk. What moves the position toward liquidation is the combination of two forces: the growing loan balance on one side and any decline in collateral value on the other. A borrower who takes out a BTC loan with a healthy buffer between the initial LTV and the 90% threshold has more room before those forces converge.

Remember that the loan balance grows every month,, regardless of market conditions, because unpaid interest compounds automatically. Over a 12-month term with no partial repayments, the effective annual cost on a 6.0% nominal BTC loan comes in just above that figure, and the LTV creeps steadily upward through the year.

But that trajectory is predictable and manageable with partial repayments or additional collateral, but we note it requires thinking it through, rather than set-and-forget behavior.

Depositing additional collateral at any point lowers the LTV and pushes the liquidation threshold further away, and that option is available throughout the loan term.

Rates and Collateral Assets

Clend’s rate structure (as per the website in June 2026):

Type

Coin examples

LTV

Liquidation LTV

Rate (per year)

Stablecoins

USDC, USDT, JPYC

90%

95%

14.40%

Major (BTC)

BTC

60%

90%

6.00%

Major (ETH)

ETH

60%

90%

7.20%

Altcoins (Tier 1)

XRP, SOL

40%

90%

8.40%

Altcoins (Tier 2)

BNB, ADA, DOGE, SHIB, MATIC, and others

40%

90%

16.80%

All rates are fixed for the duration of the loan and require no platform token to access. The 6.0% BTC rate is the lowest, and the industry average for comparable CeFi lending is around 15%, which gives a sense of where BTC and ETH rates land relative to the wider market.

Stablecoin-backed stablecoin lending – depositing USDT or USDC to borrow USDC at 14.40% – is unlikely to be the primary use case for most borrowers, but it is a utility that makes sense in specific arbitrage or treasury contexts.

Disbursement is available in USDT across five networks (ERC-20, BSC, TRON, Polygon, and Omni), USDC on ERC-20, and JPYC for Japanese market participants.

Who Should Consider Clend?

The collateral floor of approximately 33,000 USD will determine the audience, and Clend is likely not a product for someone with a mid-sized ETH wallet looking to cover a few months of expenses.

The most straightforward fit is a long-term BTC or ETH holder who needs a substantial stablecoin sum for a fixed period (e.g., a tax liability, a property transaction, a short-term investment) without wanting to sell. A large crypto sale creates a capital gains event in most countries and permanently reduces the position, but a collateralized loan avoids the disposal, preserves the full holding, and comes with a fixed rate. Again, regulations differ across the world, and we recommend Clend, but only if you’ve done your tax homework beforehand and it’s a good fit for you.

We think the second strong fit is a crypto-native business, where Web3 companies and blockchain-focused firms that carry BTC or ETH treasury balances face the same liquidity challenge as individual high-net-worth holders. Clend may be the path when using treasury assets as collateral to fund operations or growth spending.

The profile that should probably look elsewhere is anyone who might need to exit the collateral position before the loan term ends, or who cannot sustain the upward LTV drift that comes with no monthly payments over a full year.

The 61-day lock on full repayment is also worth noting: anyone who needs the entire loan resolved within the first two months after signing should account for this constraint.

Applying for a Loan

The application process runs online across four stages.

Submit an Application

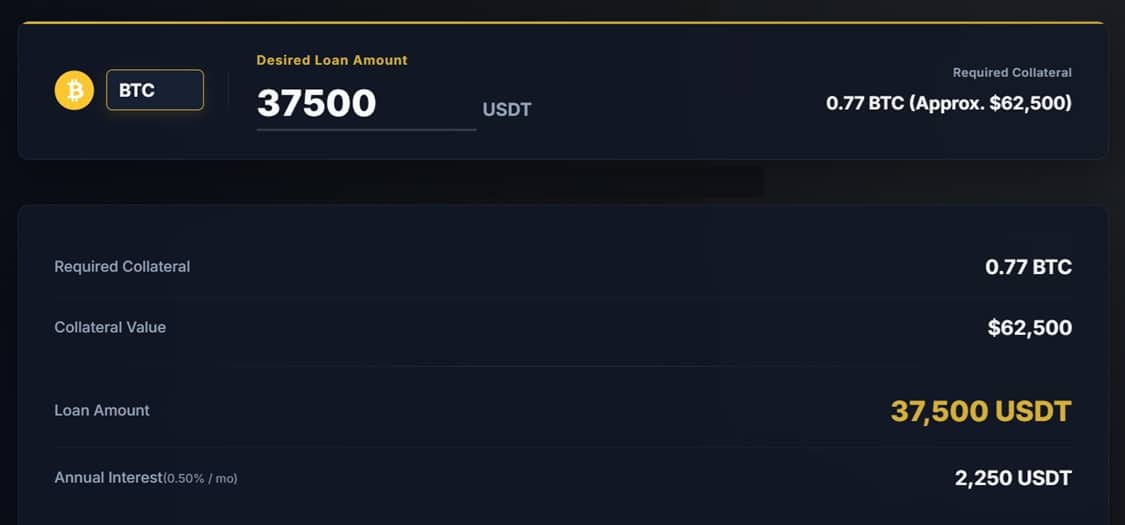

The process begins on the Clend website, where an on-site calculator lets prospective borrowers model potential loan amounts, LTVs, and approximate liquidation thresholds before committing. The application form captures the key details of the proposed loan. Clend’s team reviews the submission and returns a personalized loan proposal.

Identity Verification

KYC is mandatory for all borrowers, individual and corporate alike. The verification process runs entirely online. Documentation requirements will vary by applicant type, but the process does not require in-person attendance.

Sign the Loan Agreement

The formal agreement sets out the loan amount, annual rate, collateral asset, and maximum 12-month term. Signing happens digitally. This is when the fixed rate and all loan conditions are locked in.

Transfer Collateral and Receive Stablecoins

Collateral goes to a Fireblocks-secured address. Once the blockchain confirms the transfer, stablecoin funds are sent. Clend states that same-day settlement is possible in many cases, though confirmation speed for the specific collateral asset will affect the timeline.

There are no fees beyond the stated interest rate. Origination is free, disbursed funds incur no withdrawal fee, and early loan closing incurs no penalty, provided full repayment occurs after day 61.

Is Clend Worth Using?

For the specific borrower it is designed for, the answer is yes. The 6.0% BTC rate with a 60% LTV, no monthly payment requirement, and usually same-day stablecoin disbursement is a package that competes well in the current CeFi landscape. Fireblocks custody provides the institutional security needed when pledging a large crypto holding.

The compounding structure deserves more attention than it typically receives. A BTC loan at 6.0% nominal interest costs slightly more in effective terms, and the loan balance grows each month regardless of market movements.

The 33,000 USD minimum collateral is also a firm bottom line on accessibility. For those it excludes, Clend is simply not the right product. For those it includes, it solves a genuine problem with transparent terms and competitive pricing.

Clend is a genuinely useful crypto service that makes borrowing against your crypto as easy as possible, with great rates and high security.

Clend is operated by R0 Inc. Crypto markets are volatile. Collateral may be liquidated if LTV thresholds are reached. Tax treatment varies by jurisdiction and individual circumstance; always consult a qualified tax professional. This article does not constitute financial, legal, or investment advice.

Clend

![]()

Pros

Cons

FAQs

What is Clend?

Clend is a crypto-backed lending platform operated by New York-based R0 Inc. Users pledge digital assets as collateral in exchange for stablecoins – USDT, USDC, or JPYC – at fixed annual rates starting from 6.0% on Bitcoin, without selling their underlying holdings.

What is the minimum loan size?

The minimum loan amount is 630,000 USDC, with a minimum collateral value of approximately 33,000 USD equivalent.

How does Clend's liquidation mechanism work?

Liquidation is triggered when the total outstanding balance – original principal plus all accumulated interest – reaches 90% of the current market value of the pledged collateral. For stablecoin collateral, that threshold is 95%. Because interest accrues to the balance each month, the LTV rises gradually over the loan term, even if the collateral price stays flat. Borrowers can reduce this by making partial repayments or depositing additional collateral.

Does Clend require monthly payments?

No. Interest is not billed monthly. It accumulates and is automatically added to the loan balance each month. The full outstanding amount – principal plus all interest – is due at repayment. Partial repayments are permitted at any time; full repayment is available from day 61 after the contract is executed.

Is taking a crypto loan a taxable event?

Pledging crypto as collateral rather than selling it does not constitute a disposal in many jurisdictions, meaning no capital gains event is triggered when borrowing. Tax law varies substantially by country and individual circumstance, however, and a qualified tax professional should always be consulted before relying on this assumption.

Who is Clend most suitable for?

High-net-worth individuals holding BTC, ETH, XRP, SOL, or similar assets who need stablecoin liquidity over a defined period without selling their position. Corporate borrowers – particularly Web3 companies or crypto-native businesses with treasury holdings – are also a natural fit.

Why you can trust 99Bitcoins

Established in 2013, 99Bitcoin’s team members have been crypto experts since Bitcoin’s Early days.

Weekly Research

100k+Monthly readers

Expert contributors

2000+Crypto Projects Reviewed