3 Comments

3 CommentsThis article is based on the opinion of the author, who does not necessarily disagree with the proposition of increasing block size, but rather the recent economic reasoning used to justify it.

Gavin Andressen Proposes an Infinite Increase on the Maximum Bitcoin Block size

Within the last few days, there has been some discussion in the Bitcoin community about the possibility of increasing the maximum Bitcoin block size limit of 1 MB, which is coded into the protocol. This discussion started last week, on October 6, 2014, when Gavin Andresen—the lead computer scientist at the Bitcoin Foundation—published a post on the Foundation’s official blog. In this post, Andresen said that, in order for the Bitcoin network’s scalability to be flexible enough to accommodate for the potential transaction volume of the future, the hard limit on maximum block size needed to be increased by 50% every year.

Within the last few days, there has been some discussion in the Bitcoin community about the possibility of increasing the maximum Bitcoin block size limit of 1 MB, which is coded into the protocol. This discussion started last week, on October 6, 2014, when Gavin Andresen—the lead computer scientist at the Bitcoin Foundation—published a post on the Foundation’s official blog. In this post, Andresen said that, in order for the Bitcoin network’s scalability to be flexible enough to accommodate for the potential transaction volume of the future, the hard limit on maximum block size needed to be increased by 50% every year.

From Gavin Andresen in his post on the Foundation’s official blog:

I think the maximum block size must be increased for the same reason the limit of 21 million coins must NEVER be increased: because people were told that the system would scale up to handle lots of transactions, just as they were told that there will only ever be 21 million bitcoins.

The Bitcoin Community Responds, Gavin Fires Back

Once this blog post began circulating throughout the community, a few people came out in opposition to the idea of arbitrarily increasing the Bitcoin block size limit. Their opposition mostly came from an economic standpoint; if the Bitcoin block size limit is increased by 50% regularly, until there essentially no limit, then there would no longer be scarce space in which transactions could take place and transaction fees could potentially drop below a profitable level. If fees do drop below a profitable level, miners would shut off their machines to stop their losses and the Bitcoin network would collapse.

Once this blog post began circulating throughout the community, a few people came out in opposition to the idea of arbitrarily increasing the Bitcoin block size limit. Their opposition mostly came from an economic standpoint; if the Bitcoin block size limit is increased by 50% regularly, until there essentially no limit, then there would no longer be scarce space in which transactions could take place and transaction fees could potentially drop below a profitable level. If fees do drop below a profitable level, miners would shut off their machines to stop their losses and the Bitcoin network would collapse.

Andresen fired back at those who brought attention the the possibility of greatly diminished transaction fees. On October 16, 2014, Andresesn published another post on the Foundation’s blog, titled “Blocksize Economics.” In this post, Andresen addressed these concerns not with technical computer science jargon, but with economics. In his concise response, Gavin said:

The argument for not allowing arbitrarily large blocks: a maximum block size is necessary to create artificial scarcity so transaction fees do not drop to zero, leaving miners with no income, leading to no mining and the death of the network.

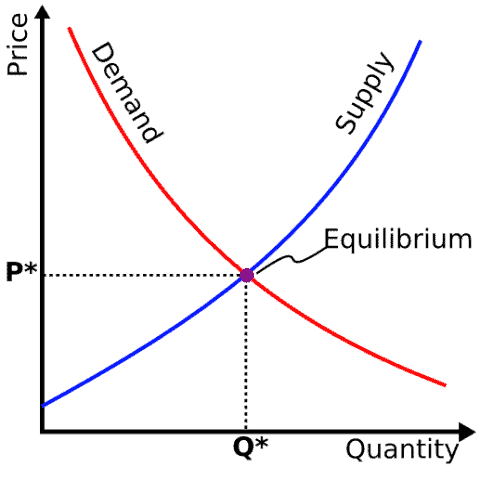

However, economic theory says that in a competitive market, supply, demand, and price will find an equilibrium where the price is equal to the marginal cost to suppliers plus some net income (because suppliers can always choose to do something more profitable with their time or money). . . So with absolutely no artificial limits to supply (like a maximum block size), transaction fees would drop to the marginal cost miners pay. . . but not zero.

Gavin’s Flawed Economic Theory Could Have a Real-World Effect on Bitcoin

As we can see, Andresen’s counterargument to the claims that an arbitrarily large Bitcoin Block size will drive transaction fees below a profitable level is simple: it is impossible for fees to drop below that profitable level because consumer prices are determined by the price of production. The only problem with Gavin’s counterargument, though, is that the economic theory he employed is incredibly flawed and has been invalidated many times over by various economists. This flaw allowed Gavin to assume that Bitcoin miners would always receive a return on their investments, because the price of their services—in this case, confirming transactions—would never fall below production costs.

This theory of the determination of prices is derives from a value theory, which is known as the cost of production theory of value. This theory is very straightforward, the value of a good comes from the cost of its production. As prices are merely a monetary denotation of value, we can easily conclude from this value theory that prices themselves are determined by the prices of the factors of production, which is precisely the conclusion that Gavin arrived at. However, prices are not actually determined by production costs.

However, prices are not actually determined by production costs.

In reality, the reverse is true; production costs are determined by the prices that consumer goods can fetch on the market. To put it back into the context of value theory: the value of a good comes from within the individual, it is subjective, and the value of the production factor comes from the value of the good that it can produce. Simply put, all value derives from the minds of individuals.

It may seem to the businessman or the person observing only a single firm that their prices are determined by their costs, but that is simply not true, for the businessman would have never taken on the task of providing this good or service, thereby paying these costs, if he did not expect to receive revenue that exceeded the cost of production (since the business man is driven by profit, he would not settle for revenue that was equal to costs). If he thought that the consumers on the market were not willing to pay a price that covered production costs and then some, then the businessman would have never made that product to begin with.

Consequently, if the consumers did not want that product at that particular price, and the businessman quit paying those production costs, the prices of the factors of production would go down as a result of reduced demand! As we can see, all prices come from the value the particular good or service renders to the consumer.

Thus, it is entirely possible that transaction fees could fall below a profitable level, in which case the miners would hang up their hats and turn off their machines. Sure, Bitcoin miners can use production costs and their desired profit margin to calculate a minimum price they are willing to charge, but that does not mean that people will actually pay that price.

The assumption on Andresen’s part that people would automatically pay those prices came from a treatment of the economy as mechanistic. Andresen held demand constant, assuming that actors on the Bitcoin network would pay whatever price for the confirmation of their transaction, and concluded that certain “mechanisms” of the market would prevent the miners from ever becoming unprofitable. But the market is not mechanistic, because humans are not machines; there are no constants, nor equilibria.

In economics, these things are used to theoretically simplify real world situations in order to better understand those situations, but it must always be remembered that these theoretical constants do not actually exist in the real world. To reiterate, it is possible for transaction fees to drop below a certain level, and they will if supply exceeds demand. Even if the miners refuse to lower their fees and opt to keep them constant, people will stop using the Bitcoin network, and the miners would become unprofitable and shut down anyway.

What Should Be Done About Bitcoin Block size?

That being said, the market would determine a “natural” limit on Bitcoin block size, even if the hard-coded limit were removed, because miners would only produce blocks small enough to ensure the transaction fees would be high enough to bring a profit.

That being said, the market would determine a “natural” limit on Bitcoin block size, even if the hard-coded limit were removed, because miners would only produce blocks small enough to ensure the transaction fees would be high enough to bring a profit.

However, this “natural” limit means that there would still be a limit on the number of transactions that can be processed on the network within a certain period of time, thereby defeating the original purpose of increasing the Bitcoin block size to facilitate a higher volume of transaction. Andresen apparently acknowledged this point and conceded to it, though, because he cited this article in the reference section of his blog post.

In light of this fact, what should be done about the hard limit on Bitcoin Block size? If the 1 MB limit stays in place, and the demand for transaction confirmations exceeds amount of possible confirmations supplied by that limit, then fees will rise and transaction volume will fall. On the other hand, if Andresen’s suggestion is implemented, and the maximum Bitcoin block size is increased by 50% every year, one of three things could happen:

Firstly, if the 50% increase is not enough to accommodate the demand for transaction confirmations, miner fees will rise and transaction volume will fall accordingly.

Secondly, if the increase exceeds the amount necessary to accommodate for confirmation demand, the market will establish its “natural” Bitcoin block size limit, due to miners only creating blocks small enough to ensure their profitability.

There is also a third, theoretical possibility, which is that the increase would be the exact amount required to bring supply and demand into equilibrium. But, as the constantly changing wants and needs of humans prevents an equilibrium from arising in the real world, this third possibility will never happen.

Either way, miners will not allow for a block with an infinite size, there will always be a limit regardless of whether or not the Bitcoin protocol mandates a limit. It is a question of economics, not computer science. Andresen can engineer the Bitcoin network and make it operate however he wants, but he cannot dictate the human reaction to those changes. He can write code, but he cannot force the direction or manner of human action.

So, returning to the question advanced above, what should be done about block size? The answer: it probably does not matter. The true Bitcoin block size will only be as large as the market allows, Andresen cannot make it larger no matter what kinds of protocol changes he implements. If he makes it too rigid, changing valuations will lead individuals to simply abandon Bitcoin; if he makes it too flexible, the market will develop “natural” regulations as individuals pursue their own self-interests.

In conclusion, Andresen’s proposed implementation of an incrementally increasing Bitcoin block size limit will be useful in preventing spam on the blockchain—which is what this original 1 MB limit was imposed for. However, as we have seen in this article, it likely will not allow Andresen to manipulate transaction volume in the way he desires. The reason being that a block size limit in excess of what is needed will lead to the emergence of a “naural” limit, imposed by the market.

In regards to network security, which Andresen refers to in the last section of his blog post, he is correct; changes to the limit on the Bitcoin block size will not solve the problem of network security. Miner fees will be determined by the market, which—as we have seen here—cannot be meaningfully influenced by changes to the protocol. This fact means that changing the block size limit cannot influence Bitcoin mining centralization, so the issue of network security must be resolved by some other measure.

I disagree that Gavin’s post implies the a cost of production theory of value. Gavin said “economic theory says that in a competitive market, supply, demand, and price will find an equilibrium where the price is equal to the marginal cost to suppliers plus some net income” Gavin does not appear to be assuming some set of fixed costs here. The condition that marginal revenue should approach marginal cost (discounted by the interest rate) is just an equilibrium condition, not an assumption about how the condition will be met. Furthermore, he says “There is no guarantee that future one-gigabyte blocks full of smaller transactions will generate enough fees to secure the blockchain.” Gavin could not have concluded this if he was assuming fixed costs from mining.

The argument about marginal revenue and marginal cost rebuts the “Transaction fee death spiral” argument that an unlimited block size will necessarily be unsustainable. It does not prove that Bitcoin will in fact be sustainable if a larger block size is allowed. Bitcoin might very will NOT be sustainable long-term when the block reward declines too much.

The real issue here is that Bitcoin is almost certainly not sustainable if the block size remains limited to 1 Mb. That isn’t something worth investing in and I don’t see how that could possibly lead to a high hash rate later on. http://bitcoinist.net/the-optimal-block-size/

That is a condition of equilibrium, indeed. However, it should be noted that the evenly rotating economy is never achieved in the real world economy, shifting demands and conditions of welfare prevent any price-determining factors from remaining constant long enough to bring the market into perfect equilibrium. That is one of the first and basic rules of Austrian economics: equilibria do not exist in the real world, they are merely theoretical constructs used to simplify real world situations. Thus, miner fees will always be above or below that equilibrium, meaning that it is very possible for fees to descend below production costs.

Which brings me to the assumption that Gavin used cost of production theory of value. He did actually say that miner fees could no go to zero because they could only fall to the marginal cost of production. For that to actually be true, the costs of production would actually have to determine prices. This is why I brought up the cost of production theory and provided a summary refutation of it. Although he was right in saying that “There is no guarantee that future one-gigabyte blocks full of smaller transactions will generate enough fees to secure the blockchain,” it cannot be denied that he did say that fees could not fall to 0 because of the costs of production. In reality, fees can fall to zero, because if no one pays the listed fee, then the market price for transaction confirmations is effectively zero. Obviously, he can’t believe in both things, so I guess that was just a lapse in thinking that no one caught.

Lastly, I never said that an unlimited blocksize would be unsustainable, I just mentioned that other people made that argument. In fact, I argued that an unlimited blocksize would ultimately give rise to a “natural” limit, since miners would only create blocks small enough to elicit a profitable transaction fee. Additionally, I agree that the limit should be raised to accommodate for increased transaction volume, as the original limit was implemented only to prevent spam on the network, and not as an attempt to engineer transaction volume or fees. All I was doing in this article was pointing out blurry economic thinking, which I believe is a very important thing to do.

read it. Was it reviewed by any actual economists? Mine was by five, are we all wrong?